Share this

by The Yes Energy Market Monitoring Team

North America is in the middle of an energy transition, ditching megawatts of coal and natural gas for more renewables, batteries, and smaller-scale energy resources. Across the US, there’s a greater focus on electrification in the consumer sectors, driving increased power consumption and the need for more effective energy infrastructure.

Along with developments in grid-scale infrastructure, we’re seeing strides in distributed energy resource (DER) technologies and participation models.

So, let’s look at what distributed energy resources are, how they can work, and what Federal Energy Regulatory Commission Order 2222 has done for DER adoption across North American power markets.

What Is a Distributed Energy Resource?

Distributed energy resources, or DERs, cover a range of resource types and technologies but are generally small-scale energy resources located off of the bulk electric system, or power grid. Common examples of DERs include rooftop solar panels, distributed wind turbines, on-site combustion turbines, batteries, and electric vehicle (EV) equipment.

In essence, a DER is an electrified piece of technology or resource operated to generate electricity, store electricity, or shift electricity demand patterns.

Strides in smart energy technology and electrification across North America have brought distributed resources closer to our communities, homes, and offices. For individuals, the goal of DER adoption is often reducing energy bills or reliance on grid supply, but with proper market design, these technologies can also benefit Independent System Operator (ISO) and retail power markets.

What Are the Benefits of Distributed Energy Resources?

DERs can offer a myriad of benefits to consumers and electricity markets. While the ISOs are working through many details of DER implementation and design, DERs can enable a more flexible and robust grid. Two DER benefits are reducing stress and costs on grid-scale supply resources and improving competition.

Creating a synchronized network of DERs can result in a more flexible and effective dispatch of resources located on and off the bulk electric system, increasing the pool of viable electricity generation to supply consumers and mitigate grid bottlenecks, especially at local levels. Electricity from DERs can also help reduce congestion costs on heavily used transmission corridors and new transmission to supply needed power. DERs offer a non-wires alternative to grid-scale power supply, reducing construction and operational costs of grid-scale resources, greenhouse gas emissions from natural gas and coal, and the lengthy time it takes to permit and interconnect new generation.

By using DERs, utilities and market operators can more effectively leverage existing energy resources to manage rapid load, voltage, and frequency changes. The flexibility and range of DER technologies can reduce the need for quick-ramping gas and oil power plants to supplement the increasing penetration of variable energy resources (VERs) like wind and solar on the grid, reducing startup and fuel costs for these types of peaker power plants.

On-site generation and storage help reduce DER owners’ dependence on the power grid and their financial risk to high prices during weather events and grid stress (like we saw during Winter Storm Uri in 2021). This enables further consumer flexibility, making wholesale electricity prices and markets more responsive and competitive. Regardless of whether DER owners use their resources for these specific benefits, DERs enable consumers to produce and consume electricity more in accord with their own needs and preferences.

What Is FERC 2222 and How Does It Impact DERs?

In 2020, the Federal Energy Regulatory Commission (FERC) mandated that ISOs develop guidelines for DER aggregations and participation under FERC Order 2222, enabling DERs to join together to become direct market participants in the broader wholesale electricity market.

Previously, DER technologies had been a viable tool for consumers to generate power or reduce demand at home (batteries are a more recent development on the consumer side), but their use in broader electricity markets was mostly limited.

FERC Order 2222 requires grid operators to develop a framework for DER participation in the wholesale energy market (WEM) as DER aggregations (DERA), establish rules for acceptable minimum DER aggregation size, and address participation models for distributed resources. Leaving the exact size requirements to the ISOs, Order 2222 established a minimum size requirement of no greater than 100 kilowatts (kW) for DER aggregations.

The FERC also left it up to the ISOs to determine and establish proper participation models for DERs. Historically, ISO markets have been designed with traditional, large-scale generation resources (coal, natural gas, etc.) and their capabilities in mind in the current electricity market framework. But Order 2222 is changing the rules of the game, allowing for entities to leverage newer, smaller, more diverse resources in broader grid operations.

Before this order, one of the primary methods DERs could participate in electricity market operations was through net-metering, a mechanism that credits energy system owners for the excess electricity they generate behind the meter and transmit onto a utility’s distribution system. This enabled DER owners to benefit financially from the excess power they generated. But with this limited participation model the wider benefits of DERs did not reach far past the distribution system.

Before Order 2222, California ISO (CAISO) was one of the earliest adopters of DER aggregation capabilities in 2016 and created a structure for DERs to be aggregated and participate in the wholesale energy market. CAISO’s existing model largely furnished the template for FERC order 2222.

FERC’s overall goal with Order 2222 is to enhance competition and help ensure that ISO markets produce just, reasonable rates. So far, ISO compliance has been somewhat of a mixed bag, with some markets finalizing implementation (CAISO) and others still working through compliance. While FERC’s order addresses DERA participation at an ISO level, a broader challenge to realize the benefits of DERs comes in the form of ISO and utility/distribution coordination.

Going forward, it will be necessary to create proper participation models and incentives across these market hierarchies so that DERs can bring their value to the bulk electric system. Market design and regulation still have a ways to go before the full value of DERs can be realized, but FERC order 2222 has opened the door for new, smaller resources and market participants to meet the needs of the power grid. One area that FERC has been very specific about, however, is how ISOs can manage and treat DER aggregations.

DER Aggregation

While individual owners can leverage DERs for personal generation, storage, or load shifting, DERs and DER aggregations above the market’s minimum size requirement (this varies by ISO) can also participate in the wholesale electric market.

To do this, individual DERs are aggregated, or pooled together, by a DER aggregator (DERA). The DERA represents the entity in charge of aggregating, implementing, and operating DER programs on behalf of the individual DER owners. Utilities are the most common candidates for aggregating DERs across their own distribution systems, but other entities can also operate DER aggregations. The DERA’s responsibilities include managing, dispatching, metering, and settling the individual DERs in its aggregation. A DERA entity can operate the distributed resources as a combined, singular unit and functions as the direct market participant for that aggregate resource in an ISO market.

While most DERs are quite small compared to traditional generating plants or grid-scale batteries, in aggregate they can operate much like these larger-scale resources, offering products (like megawatts) and services (ancillary services) into the wholesale energy market. DERAs can participate in all segments of the market: the day-ahead market, the real-time market, and ancillary services market.

Overall, the pooling of distributed resources allows DER aggregations to participate directly in ISO markets, giving consumers a new method of leveraging their own resources, indirectly participating in the electricity market, and being compensated for it.

ISO Markets and Distributed Energy Resources

California ISO (CAISO) was the first ISO to implement regulations around DERs and their participation in the ISO market, even before FERC Order 2222. CAISO began developing its rules around DERs in 2016, laying the groundwork for many of the requirements in Order 2222, including DERA participation models and a necessary minimum aggregation size for market participation

In CAISO, DER aggregations are comprised of one or more DERs with a collective rated capacity above 0.1 megawatts (100 kW). Resources above this minimum size requirement can participate in the day-ahead, real-time, and ancillary services markets. To participate in CAISO’s market, DERAs, or DER providers (DERPs) also must become, or contract, a scheduling coordinator to submit bids or offers to buy and sell energy (CAISO). Since the release of FERC Order 2222 in 2020, the amount of individual DER installations has grown dramatically, and CAISO currently has a total of seven DERAs for its market, including utility and third-party provider aggregations programs. DERs participating in a DER aggregation will no longer be eligible to participate in a utility’s net metering program.

Other North American ISOs are in the compliance process for FERC Order 2222 or developing roadmaps for implementation. CAISO leads the pack on order-specific compliance, with FERC having accepted its filing as of June 2022 and having established a timeline of implementation by no later than November 1, 2024.

MISO is by far the longest laggard, as its stakeholder and order working groups continue to draft an appropriate compliance filing to the FERC and submit an adequate timeline for implementation prior to their original implementation date of Q4 2029.

Below is an outline of the North American ISO implementation timeline (as of December 2023):

CAISO - Compliance filing accepted by the FERC as of June 16, 2022, and approved as of May 18, 2023. Full implementation is scheduled for later this year.

ISO-NE - ISO-NE’s third compliance filing was accepted by FERC on Nov 2, 2023. The implementation date is currently TBD.

MISO - Compliance and implementation timeline is currently TBD. Its previous timeline for implementation by Q4 2029 was remanded by FERC. Stakeholder groups continue to meet to develop a proper compliance and implementation timeline.

NYISO - The second compliance filing was partially accepted by the FERC on April 20, 2023. Target implementation is slated for Q4 2026.

PJM - It submitted an updated compliance filing to FERC as of September 1, 2023. It’s currently slated for Q1 2026 implementation.

SPP - It’s awaiting FERC response to their compliance filing, submitted on April 28, 2022. Current implementation is scheduled for Q3 2025.

*Timeline of implementation - NARUC Link and other sources

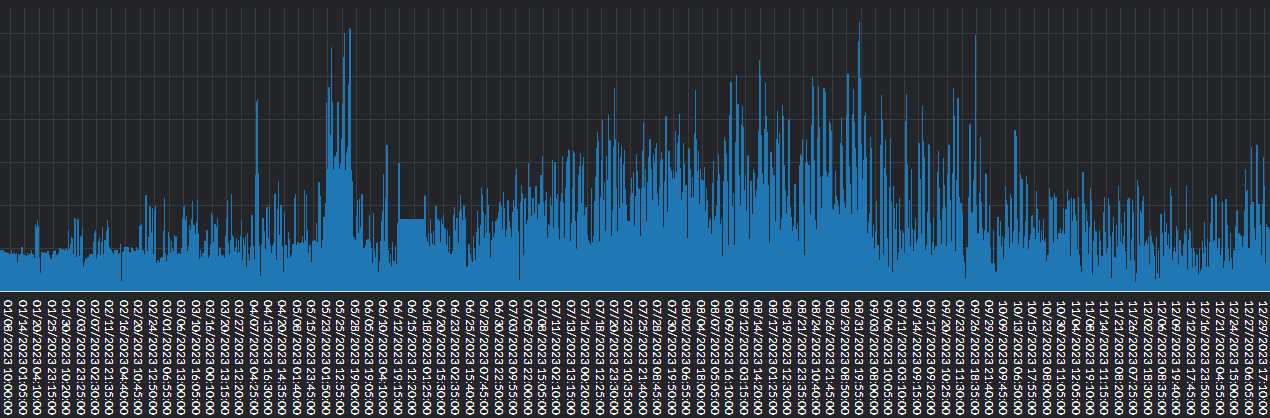

While DERs are growing, they still represent a small part of the market. For example, this chart represents the transaction volumes for 2023 for an entity participating in PJM’s Curtailment Service Providers (CSP) program through aggregated residential resources.

Source: EQR data from Yes Energy’s Transaction View

DERs and Demand Response

DERs and demand response can often look similar. However, they usually serve distinct functions in electricity markets, even if many of the technologies they operate off are similar. DERs include onsite generation, where individuals or DER aggregators can operate these distributed resources to flow power back onto the distribution system and even the bulk electric system.

On the other hand, demand response (DR) generally covers actions that electrified, distributed resources take to curtail or shift demand. The utility or market operator generally calls for these active demand reductions when there is a shortfall in electricity generation to meet load or the system is expecting some sort of stressed condition.

In short, DR focuses on flexible demand reductions, whereas DER capabilities can go even further by offering generation or stored power back to the distributor or ISO market. Many of the technologies DR and DERs operate from are the same, including battery storage, smart thermostats and EV infrastructure. Often, DERs provide the operational “hardware” for DR programs and related activities to operate on.

FERC Order 2222 defines a DER as any resource on the power distribution system, any subsystem of it or behind a customer meter … including electric storage resources, distributed generation, demand response, energy efficiency, thermal storage, and electric vehicles and their supply equipment. Based on the FERC definition, DERs include DR, electrified appliances, and other demand-side management functions like energy efficiency.

DERs are often aggregated to reach a viable level of participation in ISO markets; similarly, DR programs aggregate applicable DR technologies and behaviors to participate in managing power grid capacity shortfalls.

Overall, both DR and DERs fall under the umbrella of demand side management (DSM) and participate in energy market operations from the consumer side of the equation.

Conclusion

DERs and DERAs create new opportunities in wholesale and retail electricity markets. FERC Order 2222 has enabled DERAs to participate in WEMs, but there are still other barriers to overcome before DERs can bring their broader benefits to both ISO and retail markets.

To fully realize the benefits of distributed resources, there will need to be further coordination between ISOs, utilities, and distributors to create proper incentives at each level of electricity markets. Overall, these new, diverse, and distributed technologies enable consumers to be more proactive around their energy consumption, and in the future could change the way our current electricity markets operate.

Developments following FERC Order 2222 are prompting new players to enter power markets, and highlighting that electricity production and trading are no longer limited to large, centralized generators and retailers.

Interested in learning more about distributed energy resources and the power grid? Explore Power Generation 101.