Share this

by Portia Gilman on Jun 09, 2024

Which market regulations should independent power producers (IPPs) be aware of in 2024? Understanding policies impacting an IPP’s position in the wholesale markets and its exposure to price risk is essential.

Below is a summary of the key regulations that IPPs should pay attention to, focusing on emerging markets and regulatory policies both benefiting and challenging IPPs in 2024 and future years.

What Is an Independent Power Producer?

An IPP is any entity or company that owns and operates (and may also build) a generation resource that sells power into the wholesale energy markets.

The term “IPP” is distinct from utilities that also own and operate generation, although some IPPs were born from the deregulated entities of investor-owned utilities and therefore often share similar names (i.e., NextEra Energy).

Major players in the IPP sector include NextEra Energy, Engie, EDF, Enel, and Exelon.

Understanding the Changing Resource Mix and Load Landscape

IPPs sell electricity into the competitive deregulated markets and are therefore exposed to wholesale price fluctuations and market competition. IPPs generate a profit only if the resources in their portfolio earn energy revenues greater than the resources’ costs. This incentivizes IPPs to focus on forecasting future power prices and keeping operational costs low.

To understand why certain regulations may impact IPPs’ exposure to market risk, it’s important to consider the interplay between new regulations and key market factors driving load and generation, and therefore power prices.

The changing resource mix, and in particular the increase in variable energy resources (VERs) across all regions of the US power markets, inherently introduces additional forecast error and price volatility. Markets continue to experience deepening duck curves due to increased penetration of solar, with the timing of evening peak loads being pushed later and later in the evening. Due to increasing electrification, particularly for heating, some regions will likely shift from a summer peaking to a winter peaking system within the next few years. Depending on the severity of winter weather, this shift could happen sooner than later.

At the same time, energy storage players at the wholesale level continue to grow in number and capacity, increasing the likelihood and frequency of capturing price peaks and potentially flattening prices over time.

All of these factors contribute to an increasingly widespread demand for flexible, clean, efficient dispatchable generation to manage the changing load shape in concert with reliability concerns raised by the changing resource mix.

With these market factors in mind, what types of power market regulations are impacting IPPs in 2024?

Regulatory Benefits and Challenges to IPPs

The current regulatory landscape, particularly at the national level, is mixed with potential benefits and challenges to IPPs depending on the technologies in their portfolio.

The Inflation Reduction Act and the EPA’s recent emissions rulings provide strong incentives for the continued development of solar and other renewable resources and disincentives for gas and coal plants.

On the other hand, the Texas legislature is bolstering investment in gas-fired dispatchable generation, while higher interest rates in recent years threaten to cool investment in low-carbon technologies.

Let’s take a closer look at each of these policies.

Inflation Reduction Act

Earlier this month, the US Department of the Treasury issued long-awaited guidance concerning the applicability of the Inflation Reduction Act for solar projects. The act passed in 2022, and the solar industry had hoped for guidance by the end of 2023, which specifically addresses the 10% domestic content bonus credit, a key incentive in the act.

Per the guidance, solar, wind, and now hydro projects can receive the tax credit when the percentage of project components manufactured domestically, or the “domestic cost percentage,” meets IRS requirements ranging from 20% to 55%, depending on when construction started. The guidance also created a “safe harbor” method for developers to apply cost percentages based on classification, instead of relying on manufacturers to determine the correct calculation.

The IRS also released guidance confirming transferability of 11 clean energy tax credits in the IRA. The credits can be sold in exchange for cash to third parties who may not have a sufficient tax liability to qualify for the credits themselves. This allows businesses, governments, and tax-exempt organizations to participate and benefit from the tax credits for the construction of clean energy projects.

The initial IRS guidance provides much-needed certainty for developers and investors of renewable resources and how they stand to benefit from this lucrative tax credit. The IRS is expected to continue rolling out clarifying guidance this year.

Texas Energy Fund

This year, the Public Utility Commission of Texas (PUCT) adopted two rules implementing the “Texas Energy Fund,” a $5-billion program providing loans and grants for upgrading existing or building new dispatchable generation, primarily gas-fired plants. The Texas legislature passed a series of bills establishing the program out of growing concern for adequate, reliable capacity to meet rapidly increasing demand amidst record-breaking summers and increasing renewable penetration. The rule establishes procedures, payment schedules, and minimum performance requirements for participants to continue receiving funds annually.

The PUCT recently confirmed that generation located on private use networks are also eligible for the program, provided that 50% or more of the nameplate capacity serves the grid. Private use networks are connected to the transmission grid but contain load that the ISO isn’t directly metering because the load is netted by an on-site generation resource like a cogeneration facility.

Loan applications will take place between June 1 and July 27, 2024, with the first loans expected by the end of 2025. Grant recipients must interconnect new or expanded facilities to the grid no later than June 1, 2029, to receive the funds.

EPA Emissions Limits

In April, the Environmental Protection Agency (EPA) finalized updated rules capping emissions from newly built fossil-fuel power plants, primarily gas and baseload coal, that plan to operate past 2039. The rules require reduced carbon dioxide emissions effectively comparable to installing carbon capture sequestration (CSS) with 90% efficiency. The EPA re-defined “baseload” to include plants operating above a 40% capacity factor.

The rule also tightened the Mercury and Air Toxics Standards for emissions by 70% and tightened regulations for reducing wastewater pollution and managing coal ash.

Rule compliance begins in 2032. Notably, the rule excludes existing coal and gas plants, with the EPA expected to kick off a separate stakeholder process for regulating emissions from existing plants this year.

The EPA’s updated rule garnered pushback due to concerns that compliance requires the use of CSS technologies that aren’t yet advanced enough to support grid-scale use, potentially impacting affordability and reliability – with some utilities going so far as to say the rule is unrealistic and even unlawful. Given that legal challenges are likely, these EPA emissions rules will be important to stay abreast of in 2024 and the coming years.

Higher Interest Rates

The shift away from the zero interest rate era of recent years will impact investment and returns in the power sector, likely for the foreseeable future. Interest rates have spiked due to inflationary pressures and will likely remain high or continue to increase, resulting in a higher cost of borrowing.

The power sector in general is capital intensive, but the extent to which higher interest rates negatively impact individual projects may depend on how exposed they are to the cost of debt. Because newer, greener technologies tend to rely more on project financing and subsidies, they may be more at risk compared to equally capital intensive, but less exposed, gas and oil plants. At the same time, the energy transition will continue to increase demand, placing upward pressure on inflation.

New Markets and Services

One way that ISOs and Regional Transmission Organizations (RTOs) across the country aim to maintain reliability amidst evolving market conditions is by creating additional ancillary service markets. Let’s look at two recent examples in ERCOT and ISO New England (ISO-NE).

ERCOT Contingency Reserve Service (ECRS) and Dispatchable Reliability Reserve Service (DRRS)

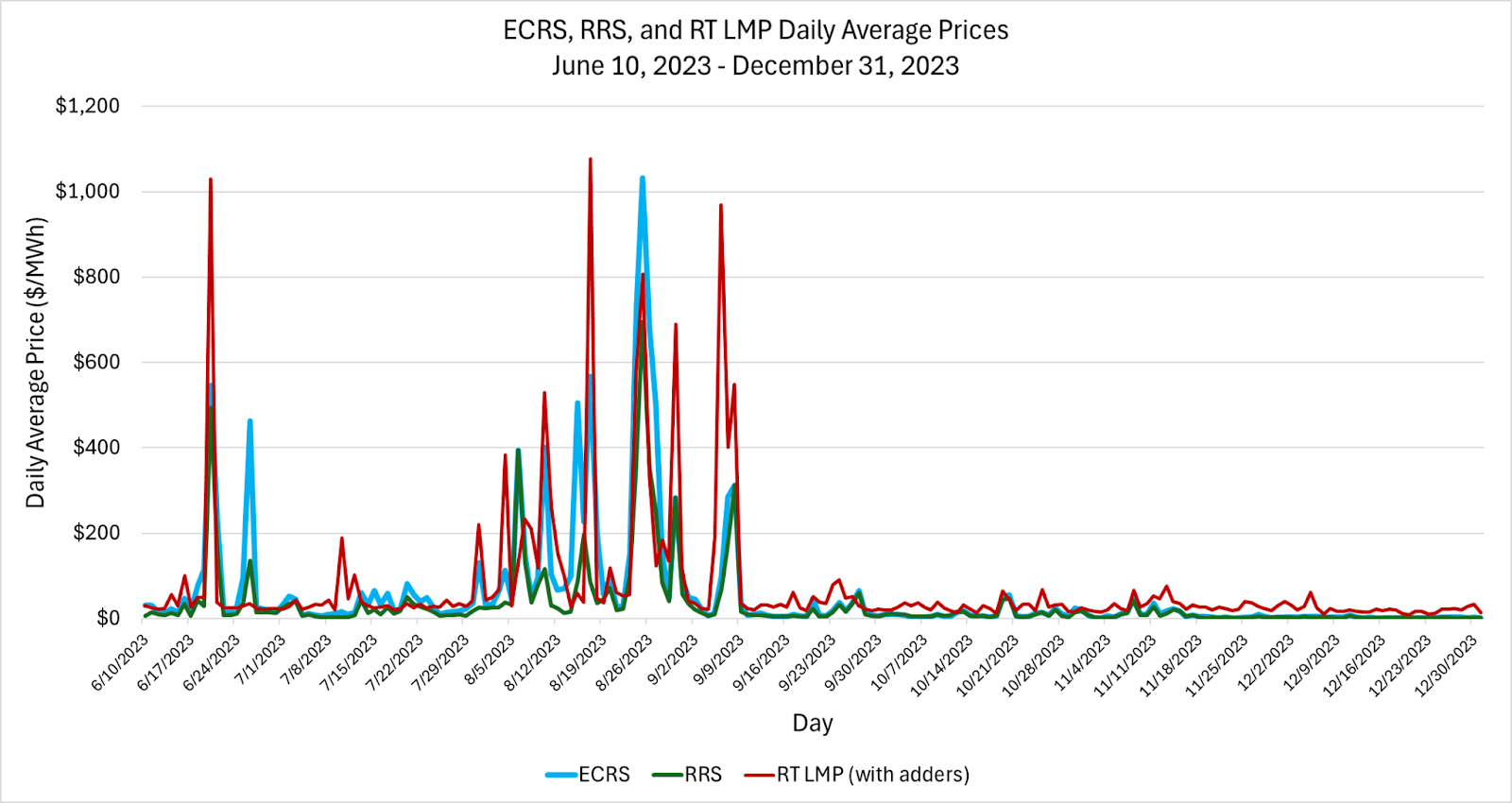

ERCOT went live with the ECRS on June 10, 2023, as an additional ancillary service tool to manage unexpected changes in grid frequency. Resources providing this service can quickly ramp in under 10 minutes and sustain output for two hours, providing a new ancillary service revenue opportunity for technologies like controllable load and energy storage resources that qualify.

By the end of 2023, ECRS came under scrutiny for its inaugural performance due to a load-record-breaking summer and significant ECRS procurement, with hourly average ECRS prices reaching as high as $4,085 on August 25, 2024.

Source: TSA

In spring 2024, ERCOT reviewed the ECRS methodology for 2024 and concluded it did not support changes to the procurement methodology but did support a change to the deployment methodology through Nodal Protocol Revision Request (NPRR) 1244. NPRR 1244 is currently moving through the stakeholder process and the Technical Advisory Committee (TAC) approved it on May 22, 2024. This rule would allow ERCOT to manually release some ECRS MWs to the SCED sooner than they did last summer, should similar conditions occur. The trigger for release is based on a Power Balance Penalty Curve violation of 40 MW consistently occurring for 10 consecutive minutes.

In its current form, the rule also includes a minimum energy offer price floor for the ECRS capacity to be no less than $750, a compromise reached during the recent TAC meeting.

The next step for NPRR 1244 is to be reviewed by the ERCOT board for approval.

For any IPPs participating in ERCOT’s ECRS, this rule will be important to keep an eye on over the next few weeks to understand how ERCOT deployment may change ECRS pricing heading into summer 2024 compared to summer 2023.

ECRS is not the only new ancillary service in the works in ERCOT. In February 2024, ERCOT began hosting workshops to discuss the forthcoming Dispatchable Reliability Reserve Service (DRRS), a new standalone ancillary service resulting from the Texas legislature’s House Bill 1500. Resources eligible to provide this service are online generation, energy storage, controllable load resources, and offline generation with a start time of two hours or less. Participants must be able to provide DRRS for four consecutive hours.

Notably, ERCOT plans to procure DRRS via the day-ahead market (DAM) and deploy during the Reliability Unit Commitment (RUC) process, but the service will not be co-optimized with energy or other ancillary services in the real-time market in the upcoming Real-Time Co-optimization (RTC) effort.

The current plan is to implement DRRS along with the RTC project or slightly after, no sooner than 2026. The regulatory development of this new ancillary service is one to watch in 2024 and 2025.

Day-Ahead Ancillary Service Initiative (DAASI, ISO-NE)

ISO-NE is moving ahead with a new Day-Ahead Ancillary Service Initiative (DAASI), which received the go-ahead from the FERC this past January. The design includes co-optimization of ancillary services in the DAM along with four brand new products: Day-Ahead Ten-Minute Spinning Reserves, Day-Ahead Ten-Minute Non-Spinning Reserves, Day-Ahead Thirty-Minute Operating Reserves, and Day-Ahead Energy Imbalance Reserve.

This design includes a novel “call option” settlement design for the new products to meet the operating reserve and load forecast requirements. In this new voluntary market, participants offer to sell the day-ahead ancillary service (DA AS), which will be cleared in the newly co-optimized DAM. For every MWh of DA AS sold, the seller will receive the DA AS clearing price and face a potential “close out” charge, which is the difference between the RT price and an ISO-determined strike price. To avoid losses, participants must respond to higher-than-expected RT prices by producing in RT to offset the close-out charge.

The idea is to incentivize generators that offer and clear the DAASI products to produce energy in RT and cover the award when conditions are tight (or when RT energy prices “call” on the resource). Implementation of the DAASI design is slated for March 2025.

In addition to energy and ancillary service markets, capacity markets also continue to evolve across the country with major developments underway, once again, in ERCOT and ISO-NE.

Performance Credit Mechanism (PCM, ERCOT)

Despite the absence of a traditional capacity market, efforts are underway to shift ERCOT away from an energy-only market environment. One of these efforts is the Performance Credit Mechanism, passed by the Public Utility Commission of Texas (PUCT) in 2023 and currently under development by ERCOT stakeholders.

The PCM is distinct from existing capacity markets in several ways, but it’s intended to address the same “missing money” problem of insufficient revenues in the energy-only market to support adequate entry (and retention) of generation resources. The program will allocate no more than $1 billion to generators for performing during the tightest hours of the year and includes familiar capacity principles like an administratively determined demand curve based on the net cost of new entry (net CONE).

What sets the program apart is that rather than being a traditional forward market run by auction, the PCM administers after-the-fact payments based on demonstrated performance, incentivizing resources to be available when they are most needed.

Many challenges remain prior to implementation, including the particulars of the program design, the overall impacts on the energy markets, and the total cost of the program. In Q1 2024 ERCOT retained Energy and Environmental Economics Inc. to work with stakeholders on the program’s design during a series of workshops. The grid operator plans to file the design with the PUCT in July 2024 with the expectation that it will issue a ruling by the end of 2024.

ISO-NE Forward Capacity Market (FCM)

A multi-year effort is underway in New England to fundamentally transform ISO-NE’s annual, three-year forward capacity market construct to a prompt/seasonal design. Alongside the shift away from large combustion turbines and combined cycle gas plants towards more renewables, the proliferation of smaller, often distribution-level, resources has rendered the three-year forward timeline obsolete.

Historically, traditional generation obtained a capacity obligation from the auction three years before the commitment period to allow sufficient time for construction and ISO compliance before coming online. Newer, smaller technologies such as distribution-level, co-located resources or even grid-scale energy storage require less time, which means that most resources participating in the capacity market no longer require three years to be built. The performance of these new resources also tends to vary more with the seasons.

Therefore, ISO-NE and stakeholders believe this new design will provide several benefits, including better accommodating development timelines of newer resources, improving demand forecast accuracy, more efficient entry and exit in each season, and improved reliability through better gas accreditation and compensation as well as alignment of the auction timelines with fuel procurement.

Last week FERC approved ISO-NE’s proposal to delay the next Forward Capacity Auction (FCA) 19, originally scheduled for 2025, until 2028 to allow time for the ISO and stakeholders to design the new capacity market. By that time, the ISO hopes to run the first “prompt” capacity auction in early 2028 for a commitment period beginning in the same year. The ISO hopes to continue reforming its capacity accreditation methodology in concert with the development of the prompt/seasonal market and so requires the additional time to ensure robust and accurate market designs.

Both the prompt/seasonal market and resource accreditation projects will fundamentally alter the participation and revenue-earning potential in New England’s most lucrative market.

One of the most exciting regulatory developments in 2024 is the race for the development of a day-ahead market in western regions that aren’t currently part of an ISO or RTO.

Western Day-Ahead Market Development

CAISO and SPP are competing for western territory in the development of independent day-ahead market proposals.

CAISO currently operates a real-time energy imbalance market (EIM) in the west and is developing a voluntary extended day-ahead market (EDAM) to build off the successes of the EIM, with implementation expected in 2026.

SPP’s ISO market operates primarily in the eastern interconnection, but also currently operates a western energy imbalance service (WEIS) market in the western interconnection. SPP is also currently developing an expanded day-ahead market in the west, via its Markets+ tariff, which the ISO filed with FERC on March 3, 2024. Thirty-eight entities across Western states participated in the development process, and the expected go-live date is 2027.

In addition to the efforts competing for a western day-ahead market, the “West-Wide Governance Pathways Initiative” is implementing step one this year in an endeavor to develop an independent regional organization to oversee both the CAISO WEIM and the EDAM, possibly paving the way for a full-fledged transmission operator (RTO) in the west.

In 2024, the first step is to continue shifting governance of the EIM away from the primarily CAISO-focused board before creating an independent organization to oversee the EIM and upcoming EDAM by the end of this year. The goal is to find a feasible framework for governing the expanded markets where previous efforts failed.

Separately, SPP ISO itself is also currently seeking to implement a western RTO in 2024. SPP’s “RTO West” initiative is an expansion of the ISO’s full market offerings into the western interconnection into states like Colorado and Wyoming. Building on the existing WEIS and the developing Markets+ frameworks, the RTO West would be the culmination of these market design efforts resulting in a full fledged RTO operating a fully functional RT and DA market in the west.

While all eyes are on the west to see which markets emerge first and which western utilities choose to participate in which markets, these parallel efforts also introduce potential challenges to interregional coordination by creating “seams” between the new day-ahead market regions. Particularly in California, which frequently relies on imports from neighboring balancing authorities when conditions are tight, the expansion of SPP’s Markets+ could impact the trade and flow of power between California and other neighboring regions.

As a recent case in point, New Mexico in May 2024 commissioned a study of the transfer capability available under the two competing day-ahead market designs before deciding which market to join. Transfer capability and transmission rights in each market are especially important for states like New Mexico, which is building merchant transmission lines to export wind power to states like California. The study’s results are expected this summer.

Another key player in the west, the Bonneville Power Administration (BPA), may have a significant impact on the success of either Markets+ or the EDAM, depending on which market they choose to go with. The BPA sells hydropower from the Northwest to municipal utilities and cooperatives and also operates 15,000 miles of transmission lines in the west.

In a recent study conducted by the Western Markets Exploratory Group, BPA confirmed that joining a day-ahead market would be beneficial, but independent governance remains a primary concern. BPA believes that the EDAM is potentially still too closely tied to the state of California and is leaning towards Markets+ as the best option for a more equitable market structure. BPA is expected to make a final decision this November.

Conclusion

In 2024, the regulatory landscape is a mix of competing factors impacting investment and development for IPPs. Awareness of these policies and the ways in which they interact with the power markets is necessary to assess the directional impact that each regulation may have on your business. The direction of impact will largely depend on the mix of technologies in an IPP’s portfolio.

At the federal level, the IRA tax credits and credit transferability, along with the EPA’s most recent ruling on emissions limits, provide a strong signal for continued investment in low-carbon renewable resources over traditional thermal plants. By the same token, the increased demand for renewables in an already high-interest rate environment puts pressure on the financeability of those very same technologies.

At the state and ISO level, grid operators grapple with the reliability challenges presented by growing renewables and the evolving load shape. Many recognize that some degree of accompanying dispatchable peaker generation may be needed for the energy transition, with some high-renewables states like Texas expected to directly subsidize new gas generation over the next several years. New ancillary services are also emerging to combat reliability concerns, providing new revenue opportunities for savvy wholesale market participants like IPPs who understand how to operate and make money in the energy markets.

Understanding key regulations in 2024 may highlight opportunities for mitigating risk for your business.

Yes Energy’s market experts and premium suite of power market data offerings are here to help you keep abreast of key regulatory changes potentially impacting your investment strategy.

Or take a look at how we're adding new data to our products to help IPPs and asset operators.