Share this

by Daniel Cullen on Aug 05, 2024

Concerned about the levels of risk relative to returns in your financial transmission rights (FTR) portfolios? As an FTR energy trader, it can be challenging to analyze and assess your portfolio relative to all other market participants to benchmark and confirm alpha returns.

The capital asset pricing model provides a framework to measure and reflect the expected rate of return for a given level of risk. It’s a financial model that establishes a linear relationship between the risk-free rate and an asset’s risk premium to give an indication of systematic risk.

What Are Financial Transmission Rights (FTRs)?

Financial transmission rights (FTRs) are financial contracts that let participants hedge potential losses related to delivering energy on the power grid. FTRs entitle their owners to compensation when the transmission grid is congested in the day-ahead power market. Given the volatile nature of power prices and transmission congestion, evaluating the risk and return associated with trading FTRs is crucial. The capital asset pricing model (CAPM) offers an effective framework for this evaluation, providing insights into expected returns relative to the associated risks.

FTRs entitle the holder to receive or pay the price difference (congestion cost) between two specified nodes in the power grid over a designated time frame. These instruments are vital for hedging against unpredictable congestion costs, ensuring more stable financial outcomes for power market participants such as generators, suppliers, and large consumers.

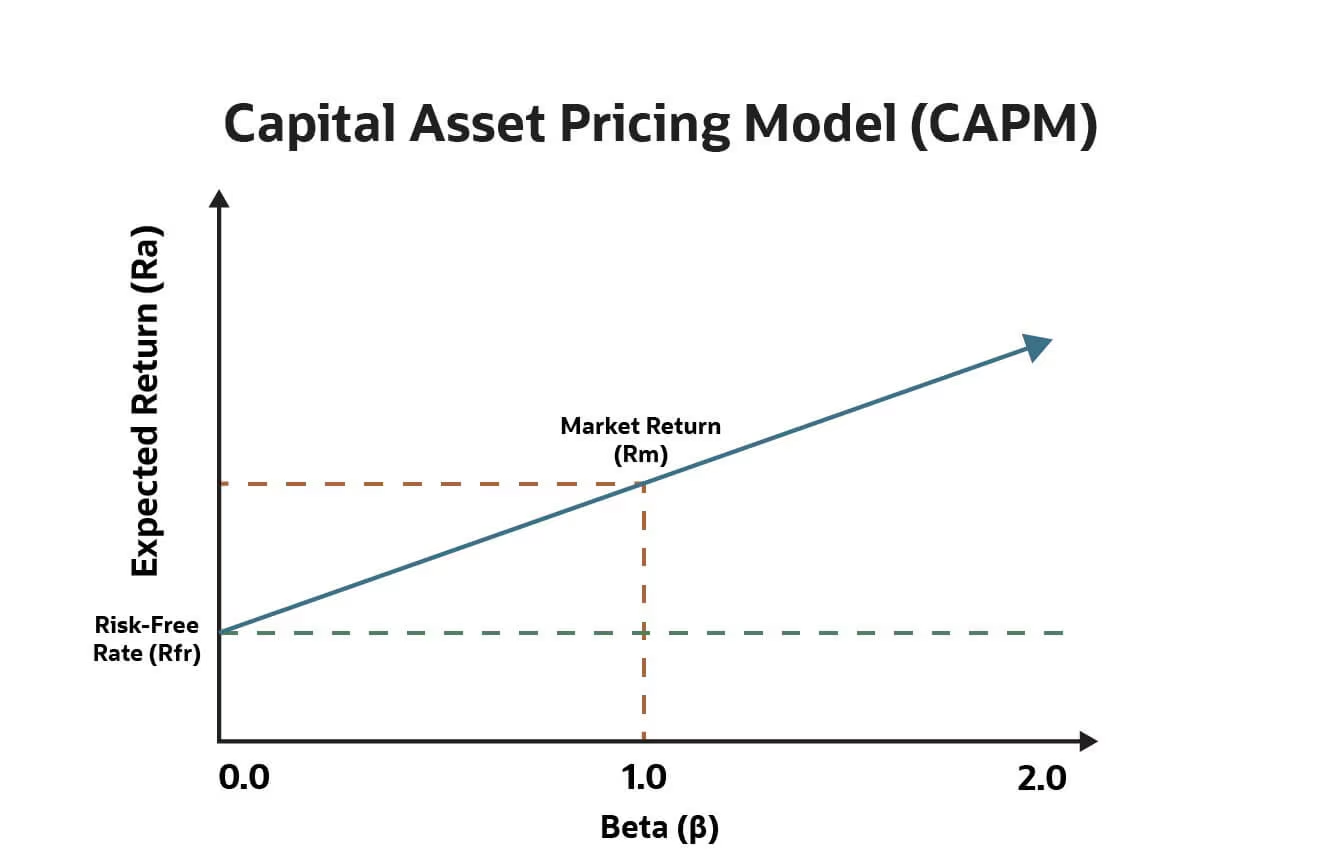

What Is the Capital Asset Pricing Model (CAPM)?

The capital asset pricing model (CAPM) is a financial model that describes the relationship between systematic risk and expected return for assets, particularly stocks. The model is expressed as:

Source: NetSuite

\[ E(R_i) = R_f + \beta_i (E(R_m) - R_f) \]

where:

- \( E(R_i) \) is the expected return on the asset.

- \( R_f \) is the risk-free rate of return.

- \( \beta_i \) is the beta of the asset, a measure of its systematic risk.

- \( E(R_m) \) is the expected return of the market.

- \( (E(R_m) - R_f) \) is the market risk premium.

The CAPM posits that an asset's expected return is proportional to its systematic risk, represented by the beta coefficient, which compares the asset's volatility to that of the market.

In the context of FTRs, systematic risk refers to the market-wide risks that affect electricity prices and transmission congestion, such as changes in fuel prices, regulatory shifts, and macroeconomic factors. FTRs are exposed to these risks because they’re linked to the congestion costs resulting from the overall supply and demand dynamics in power markets.

To apply CAPM to FTRs, we need to estimate the beta (\( \beta \)) for these instruments. You can determine the beta by analyzing historical data on FTR prices and comparing them with a broad index of electricity market performance, such as the locational marginal prices (LMPs) in the power grid. You can use statistical methods, such as regression analysis, to find the relationship between FTR returns and overall market returns.

Once you estimate the beta, you can use the CAPM formula to calculate the expected return on FTRs. You can approximate the risk-free rate (\( R_f \)) using the return on government bonds, while you can derive the market risk premium (\( E(R_m) - R_f \)) from the historical performance of the electricity market.

The CAPM allows you to evaluate the risk-adjusted performance of FTRs by comparing the expected return to the actual return. If the actual return exceeds the expected return calculated using CAPM, the FTR is providing a higher return for its level of systematic risk, making it an attractive investment. Conversely, if the actual return is lower than the expected return, the FTR may be overvalued relative to its risk.

You can effectively apply the CAPM model applied with leveraging the FTR Positions Dataset (FPD) to assess the optimal balance of performance and risk within and across ISO markets of your positions.

While CAPM provides a valuable framework for evaluating the risk and return of FTRs, you should also consider other factors:

- Liquidity: FTR markets may lack the liquidity of more traditional financial markets, affecting the ease with which you can enter or exit positions .

- Regulatory Environment: Changes in regulations governing power markets can have significant impacts on FTR valuations.

- Operational Risks: Issues such as grid reliability, maintenance, and unforeseen outages can affect transmission congestion and FTR payouts.

Conclusion

The CAPM is a powerful tool for evaluating the risk and return of trading FTRs in power markets. By quantifying the systematic risk associated with FTRs and estimating their expected returns, CAPM helps you make informed decisions.

However, it’s essential to consider additional market-specific factors to fully understand and manage the complexities of trading FTRs. By carefully applying CAPM and a comprehensive risk management strategy, you can better navigate the uncertainties inherent in power markets.

Yes Energy Can Help with FTR Energy Trading

Yes Energy’s FTR Positions Dataset solution provides FTR energy trading organizations and regulators with unprecedented visibility into FTR market positions. Historically, only FTR trading organizations with large IT budgets have been able to build systems to gain visibility into the positions, performance, and risk of their competitors in the market. With FTR Positions Dataset, you can outsource this expensive data management, including trade capture, model remappings, and ISO changes.

You can do the following in our FTR Positions Dataset:

- See all positions in US FTR markets.

- Use industry-standard methodology for marking and settling FTR positions, providing contract level closed (realized) and open (mark to market) profit and loss data.

- Use standardized risk metrics to compare risk usage across markets and participants.

We deliver all of this on the powerful Snowflake cloud platform. (Snowflake is a data warehouse available across multiple cloud regions). This allows you to answer the above questions in seconds, compared to a more manual process that may take hours or even days for each auction.

You can also further integrate this data with Yes Energy’s DataSignalsTM Cloud datasets, internal data, and other third-party data available on Snowflake, fueling powerful big data analysis.

Learn more about the FTR Positions Dataset today, or request a demo.

About the Author: Daniel Cullen has more than 10 years' experience in commodity and power markets. The majority of that experience focused on the development and delivery of performance and risk solutions. At Yes Energy, he serves as the product manager for Submission Services, Position Management, and FTR Positions Dataset.