Share this

by Rob Strange

Winter has arrived, once again testing the reliability of the grid and resource adequacy on the eastern seaboard.

Amid the energy transition, reliability risk is shifting from the summer to winter months. Winter load is becoming more sensitive to ambient temperature and extreme weather events. The winter net peak is expected to be higher and flatter, driven by the electrification of heating in homes and businesses.

This extended peak creates risks, as supply must sustain high demand to avoid significant load loss.

Independent System Operators and Regional Transmission Organizations (ISO and RTOs) along the eastern seaboard currently face challenges due to projections of lower reserve margins. While the collective anticipated reserve margins should be enough to maintain reliability during the winter season of 2024/2025, optimizing thermal generation will be crucial as these margins decrease.

The winter of 2024/2025 presents an opportunity for the market to implement the lessons learned from 2022 Winter Storm Elliot. Although last winter was relatively mild, it still provided electric markets with valuable insights gained from past extreme weather events.

The ISO markets are responding quickly to avoid widespread loss of load and price spikes during cold snaps. There are ongoing challenges to accredit resources that will show up in the winter season, mitigate price scarcity, and improve gas-electric coordination. This multi-faceted issue is critical for understanding how the electric system will evolve and shape reliability standards.

Explore how system operators are working to improve winter reliability, including using effective load carrying capacity.

Accrediting Resources That Improve Winter Reliability

Why do we continue to invest significantly in natural gas?

During the winter, shorter days and increased cloud coverage limit solar energy generation and hybrid systems' ability to charge and discharge energy storage.

In contrast, cold snaps often result in strong winds along the eastern seaboard, creating significant potential for offshore wind resources. As capacity markets undergo reform to enhance reliability, participants are adapting to respond to new market signals.

Resources in the eastern RTOs competitively sell capacity in a centralized capacity market. The RTO determines the amount of reliable capacity required to meet system peak conditions known as the planning reserve margin (PRM). Resources will competitively offer capacity until the PRM is met, and all resources will be awarded the clearing price that the last marginal unit bids.

However, stakeholders have focused on determining how much capacity a resource class can bid into the market. Capacity accreditation awards resources that perform better in the hours of risk where supply can have a large loss of load, making thermal generation a more reliable resource than most intermittent renewable resources.

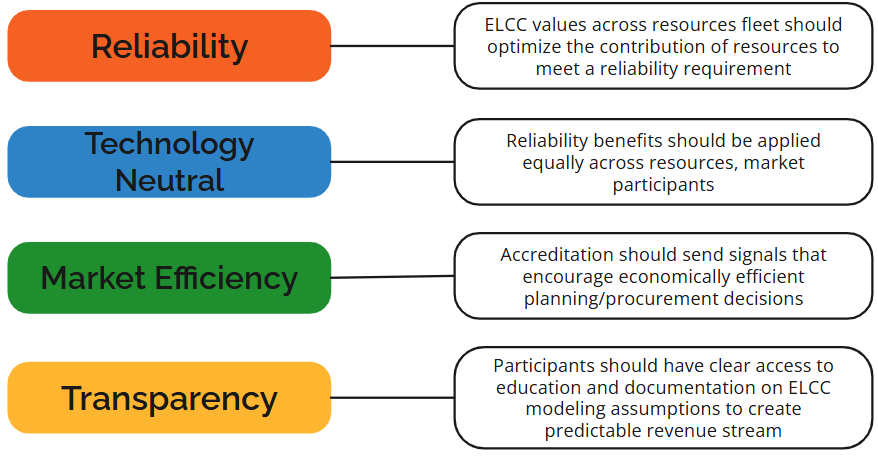

What Is Effective Load Carrying Capability (ELCC) and Why Use It?

The RTOs and stakeholders are learning how to apply effective load carrying capability (ELCC).

ELCC is an accreditation methodology using probabilistic models to quantify resource performance during stress conditions associated with weather conditions and ambient temperatures. The model will optimize the resource mix to meet the reliability standard of loss of load expectation (LOLE) of less than one day of outages in ten years.

ELCC has gained traction with the higher proliferation of renewable resources, subjecting both renewables and thermal resources to the ELCC accreditation process. Historically, thermal generation was measured by equivalent forced outage rate demand (EFORd) and unforced capacity (UCAP), which outputs the annual average rate of outages.

However, the annual average has masked the higher risks associated with winter conditions. By shifting to ELCC, capacity markets will improve signals to better address winter risk as opposed to annual average rates. Reliability during cold weather events can impact the availability of fuel supply and generator performance and vary load profiles that are masked when applying the annual averages.

The Pennsylvania-New Jersey-Maryland Interconnection (PJM) is now applying ELCC methodology to the performance of thermal and variable generation across the entire fleet. ISO New England (ISO-NE) is also reforming its capacity auctions to better accommodate winter risk challenges.

Though each ELCC methodology will differ across ISOs, the founding principles are the same. RTO transparency and education will be critical as RTOs roll out ELCC methodology to operations.

Source: Yes Energy

As capacity markets evolve to include ELCC, stakeholders debate how best to model correlated outages. Unexpected loss of load can result from equipment performance issues or larger events that simultaneously trigger outages across generation units and transmission systems.

The ELCC models these events, known as correlated outages, to account for loss of load coincident with temperature. ELCC may include or exclude correlated outages when assessing a resource’s reliability. The results of these modeling decisions will influence how the system hedges risk and invests in winterization efforts.

Annual capacity auctions are also subject to change so they can correspond with seasonal ELCC ratings. Annual auctions can send confusing market signals about how capacity resources should respond across the year and whether their contributions to reliability will be rewarded. ELCC values are effective when they reflect individual seasons, not overall annual accreditation. The seasonal ELCC value will support seasonal auctions that will send clearer market signals and the resource's contributions toward reliability.

ELCC Could Create Market Efficiency Uncertainty

ELCC will enhance the capacity market’s ability to assess winter risk conditions for each resource class. An ELCC rating determines the quantity of capacity a resource can bid in auctions, with revenue earned upon delivering accredited MWs and penalties for not meeting the rating.

However, the ELCC methodology creates uncertainty in generating units' responses to performance ratings. Even if ELCC models represent characteristics that a resource class can explicitly improve, it’s not likely to incentivize winterizing components or adding storage for renewable resources. This could lead to increased costs without improving the amount of megawatts (MW) that entities can bid in the next capacity auction.

When seeking returns on their investments, resource owners face a tough choice between investing in the weatherization of existing assets or developing new resources with higher ELCC ratings. Auction prices can be complex and may not signal clearly whether to upgrade current assets or pursue new developments. Since ELCC is based on ex-ante modeling and relies on historical data, owners must accept performance expectations and the consequences of past events.

A capacity market participant’s net revenue will shift from overall performance to performance during scarcity emergency conditions. The ELCC rating could compromise the unit’s ability to respond to energy prices if that unit has a fixed commitment. The ELCC values might not strongly motivate generation owners to improve winter reliability beyond their ratings. Performance bonuses may drive some investment in retrofit enhancements that improve performance beyond the initial ELCC rating.

ELCC values will place pressure on conventional generation to invest in maintaining reliability during winter months. If the ELCC and other reforms lead to more accurate clearing prices in capacity auctions, it could improve the signal to aging thermal generators to retire when cheaper, lower-cost renewable resources are providing adequate reliability. For a better understanding of how PJM’s resource stack is affected by reliability planning and policy factors, refer to the previous blog, What to Know About PJM Plant Retirements.

Reserve Products Mitigate Price Spikes

As ELCC quantifies the risk of loss of load during winter conditions, winter risk also includes vulnerability to price scarcity conditions. Even when forced outages don't occur, the natural gas system can still be highly constrained, leading to high natural gas prices and contributing to scarcity pricing in the energy market. Generators may not react in real time to spikes in load because of high gas prices.

The capacity markets aren’t the only place reform is happening at the ISOs – PJM and ISO-NE are also making changes to ancillary services markets. These changes will generate reserve market signals, incentivizing better preparedness for stress conditions and enhancing fuel security as well as improving reserve and reactive power capabilities

Resources’ reserve capability improves reliability but isn’t efficient when it happens only in the real-time (RT) market. Resources that respond to emergency conditions in the RT market may not respond in time, and may even be penalized, if the system operator commits them too late. Making fuel arrangements is also difficult if the system operator doesn’t commit the unit in time. The cost of reliability should be reflected in the day-ahead market in the optimization engine. Establishing day-ahead ancillary markets should help align fuel procurement and enhance generator preparedness, reducing the reliance on out-of-market actions.

With the right market mechanisms in place, the generator will be incentivized by the operating reserve clearing price or credit system that adds liquidity to make “just in time” gas commodity purchases. This boosts confidence for gas marketers to respond to and potentially update their contracts with generators, which reflect market mechanisms.

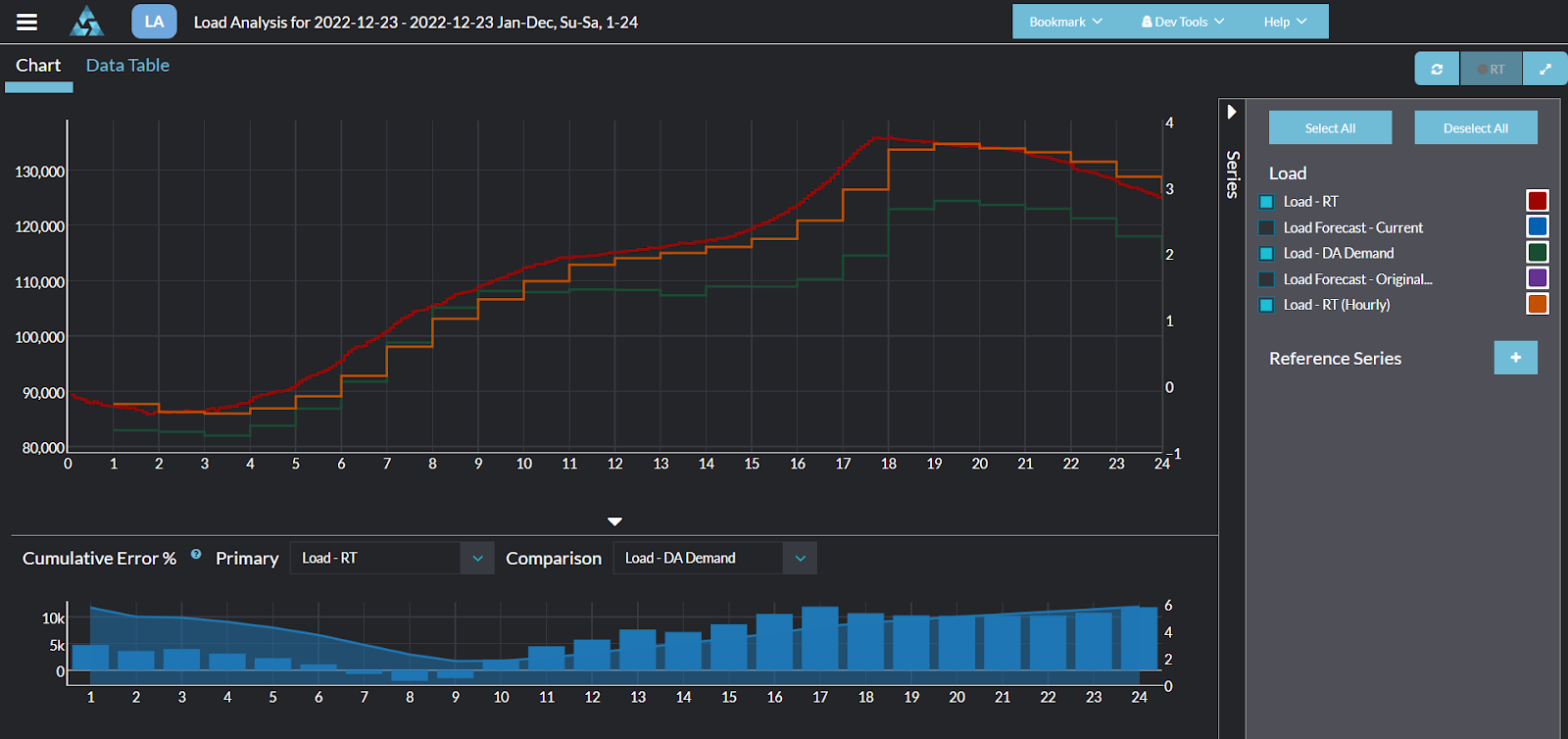

The graph below shows the conditions during Winter Storm Elliot in PJM, highlighting the day-ahead energy gap cumulative error reached nearly 6%. In this scenario, resources would have to quickly commit to procure fuel to meet demand. Without the right financial products, generation will struggle to close the energy gap without incurring losses when the day-ahead obligations cannot meet the load. The reserve market can efficiently address the day-ahead energy gap and mechanisms to procure fuel reserves during scarcity pricing. While this example shows extreme conditions, typical winter peaks can still last four to five hours in the evening.

Source: Yes Energy’s PowerSignals Load Analysis

Efforts to Improve Gas-Electric Coordination

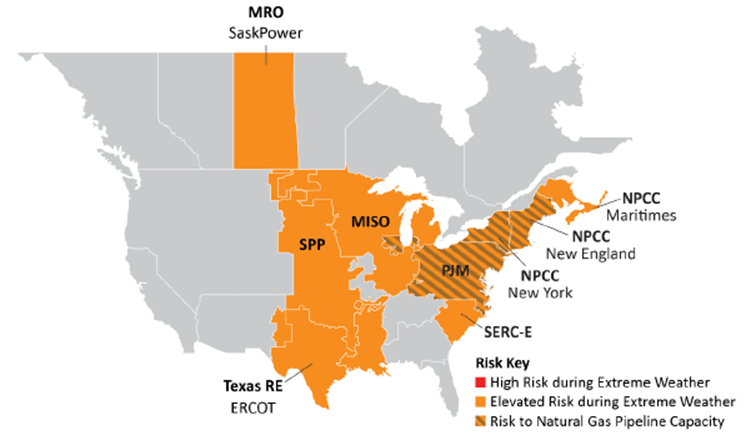

In addition to internal efforts to address increasing winter risk, there’s also been increased effort to improve gas-electric coordination. As illustrated in NERC's Winter Reliability Assessment map, the capacity of natural gas pipelines is a significant risk affecting PJM, NYISO, and ISO-NE.

Source: NERC’s Risk Winter Assessment

Gas constraints and pipeline capacity issues pose significant risks in the US Mid-Atlantic and Northeast. However, these broader objectives are being addressed at the federal level. Optimizing electric and gas operations requires coordinated oversight from regional, state, and federal authorities, along with an understanding of their interrelationships for effective regulatory processes and infrastructure planning.

Understanding current improvements across the two industries in scheduling, transparency, and infrastructure can help Yes Energy users understand price formation in winter conditions and the uncertainty of natural gas supply. As natural gas often sets the price during winter conditions, the lack of gas-electric coordination increases scarcity pricing across the region’s locational marginal prices (LMPs) as well as constraints when natural gas combined cycle plants shut down.

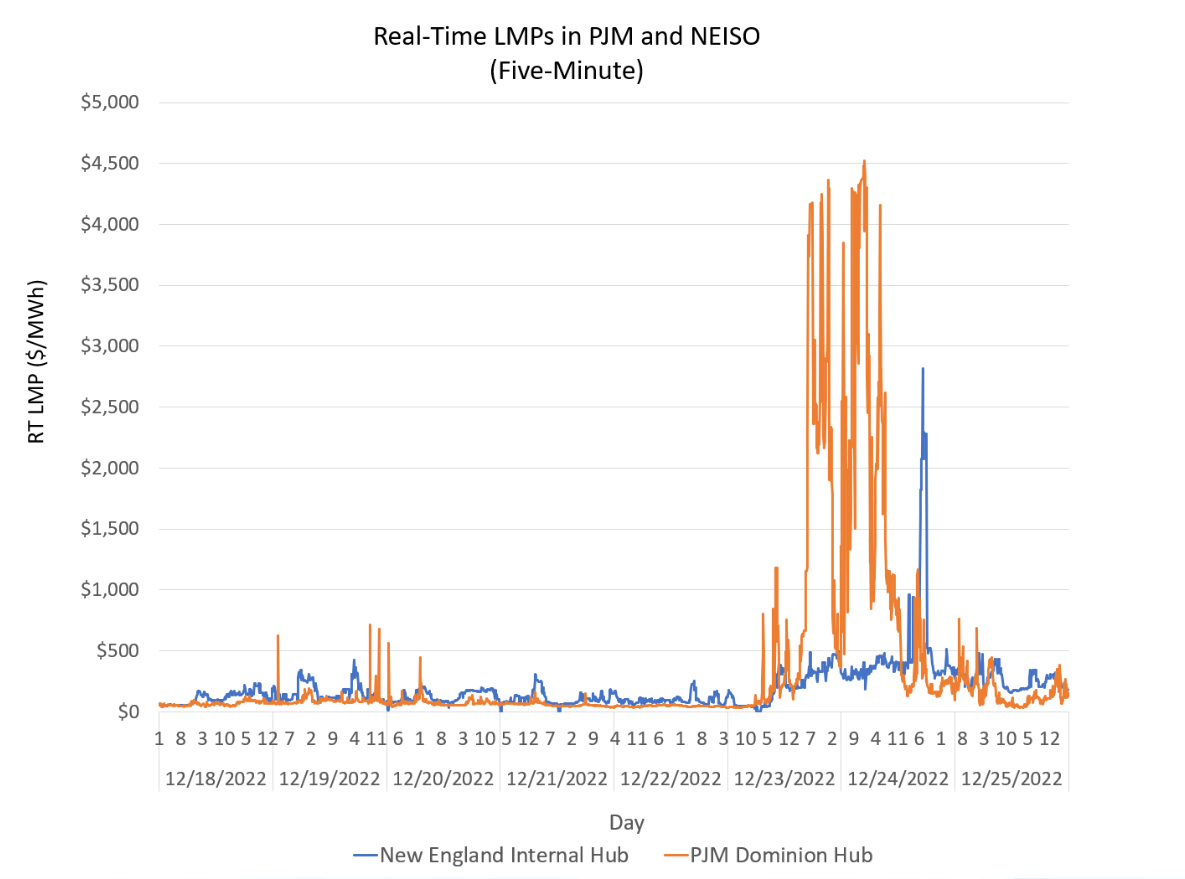

Breaking down past events like Storm Elliot in 2022 can help us understand how gas constraints and price security occur.

As seen below, the price reflects price scarcity conditions influenced by natural gas constraints. ISO-NE hub max price is nearly $3,000/MWh and PJM hub max reaches $4,500/MWh.

Source: Yes Energy’s PowerSignals

How to Improve Scheduling and Transparency

Gas systems can be quickly constrained when last-minute scheduling occurs. Natural gas markets preferably rely on long-term contracts to secure rates and transportation, while reserve and peaking plants need scheduling flexibility and market liquidity. Reforms in fuel procurement policies will improve market efficiency in both sectors.

Currently, gas marketers operate in a secondary market with limited transparency, relying on local distribution companies (LDCs) that also lack oversight.

Gas has a higher likelihood of seeing constraints during weekends and holidays. Gas marketers have a tradition of multiday trading in the secondary market, which complicates alignment between electricity day-ahead markets and natural gas purchased one to three days earlier. Extreme conditions over weekends or holidays can increase vulnerability to outages and scarcity pricing. If pipelines accepted daily trades, the electric system could respond more quickly to market changes.

Price spikes are often set from the fuel procurement of last-minute dispatch or fuel shortages. Improving flexible scheduling and transparency would help market participants make better-informed decisions that would mitigate price volatility and stabilize prices. LMPs can better reflect the costs of generation if gas availability is more predictable and aligned with electricity dispatch during price spikes.

How to Improve Infrastructure and Hedge Risk

Gas constraints also occur because gas infrastructure expansion and performance improvements happen separately from electric grid planning. Independent gas pipeline and electric grid planning hinders cost-effective solutions to address congestion. Modeling the relationships between future natural gas demands and specific congestion points can guide infrastructure expansion decisions.

Inadequate winterization of natural gas infrastructure can lead to correlated outages when gas wellheads freeze. Natural gas suppliers aren’t mandated to winterize equipment, leaving generators to bear most of the risks. This results in weak signals for improvements in readiness and winterization investments, which can be reflected in the accreditation process or market clearing.

By strengthening gas systems, electric markets can reduce supply bottlenecks and lower volatility in gas prices, leading to more stable market conditions. Shifting the risk from power generation to local distribution companies (LDCs) can enhance winterization efforts, improving market signals for necessary investments in upstream facilities.

Conclusion

Winter risks and gas constraints will likely rise with increasing demand and extreme weather events. However, balancing stakeholder engagement and timely actions can mitigate these risks and meet loss of load expectations (LOLE) through improved electric market design and enhanced gas-electric coordination. Market design changes happen frequently.

Without adequate advance notice and the market knowledge required to understand the changes, market participants risk being caught off guard.

Yes Energy can help anticipate how specific ISO/RTO markets adapt to winter risks and reliability standards. The interconnectedness of energy, capacity, and ancillary markets influences both day-ahead and real-time operations. As market designs evolve to address reliability under future conditions, Yes Energy provides analytics to clarify market signals, helping market participants make informed investment decisions and navigate market complexities effectively.

Staying abreast of the various ISO market knowledge and understanding of different markets can be time-consuming and often feels like navigating a black box. Yes Energy’s market monitoring services can help mitigate this uncertainty by empowering customers with the knowledge necessary to understand the impacts of market design changes.

About the author: Rob Strange has over 10 years of experience in analytics and product development for energy solutions. His specializations include integrated DER grid benefits and resource planning by modeling grid capacity, economic conditions, and end-use characteristics. Rob is a senior market analyst on the market monitoring team at Yes Energy, leveraging his analytic experience to track and evaluate how regulatory changes impact energy market data and related market signals.