Share this

by Gaby Flores on Dec 09, 2020

If you need to catch up, read the Power Markets 101 series.

We’ve come a long way learning about the grid, the history of US power and ISOs, the dual-settlement market, and electricity generation basics. In our last two installments, we’ll dive into the financial markets. In this one, we’ll discuss the purpose of financial power markets and their structure.

Learn about:

- SCED (security-constrained economic dispatch)

- Physical vs. financial power market participants

- How financial participants facilitate:

- Liquidity

- Hedging

- Price convergence

- Market efficiency

- Risk mitigation

Financial Markets, Economic Efficiency, and Security-Constrained Economic Dispatch

Financial markets are a unique aspect of deregulated power markets. When FERC deregulated power markets, people created ISOs and RTOs to offset the natural monopolies resulting from vertically integrated utilities.

In regulated markets where utilities have a natural monopoly, their primary mandate is to provide reliable electricity. Economic efficiency is not their primary concern.

In fact, utilities are guaranteed a set percentage of profit on their spending, so in some cases, they may actually be incentivized to spend money and resources in a way that isn't necessarily economically efficient.

However, in deregulated markets ISOs exist to dispatch generation and deliver electricity in the most efficient and economical way possible. SCED (security-constrained economic dispatch) is one of the ways that ISOs accomplish this. ISOs use sophisticated computer systems to monitor the grid and send out signals, dispatching generating units much more efficiently than human dispatchers.

SCED dispatches electricity generation that physical participants own. Physical participants buy or sell actual electricity, and they have a physical need to use the power grid and transmission services. They are often utilities, load-serving entities (LSEs), or independent power producers (IPPs).

Liquidity

The other way ISOs and RTOs achieve their mandate of economic efficiency is through financial participants. Financial participants don't own generation to supply electricity nor do they intend to remove large amounts of electricity from the grid. Financial participants primarily provide liquidity in the markets.

Markets are only liquid if there is someone to buy a product or asset, and the value of the product is not truly determined until someone sells it.

Allowing financial participants to take part in the markets helps to ensure that there are plenty of buyers and sellers in the markets, providing liquidity.

Hedging and Price Convergence

Financial markets are also a mechanism for hedging. Hedging allows market participants to offset the risk of another position they have taken. Financial markets provide a way for physical asset owners to hedge.

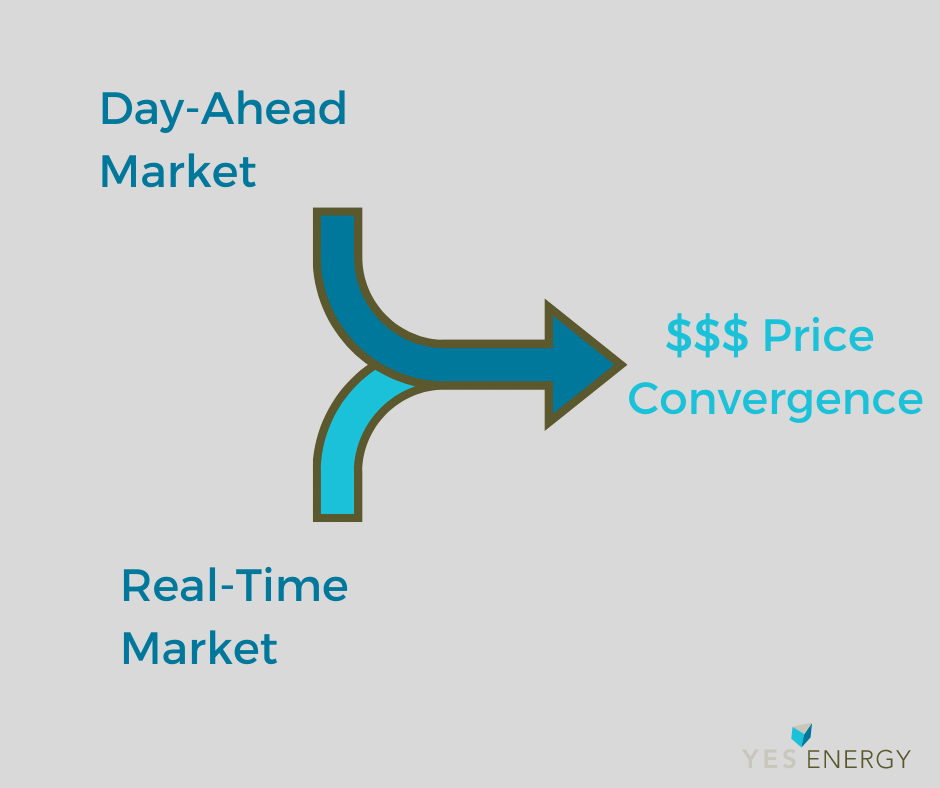

Allowing financial traders to participate in the markets also encourages further competition, which helps lead to price convergence. Ideally, ISOs want the day-ahead market to match the real-time market exactly, which would result in price convergence. Financial traders identify inefficiencies in the market, moving the ISO closer to that price convergence.

Financial traders also serve the purpose of assuming some of the risk involved. In a way, they are providing insurance to other market participants. Learn how professionals become energy traders and the role they serve in power markets.

In summary, by allowing financial participants to take part in the markets, ISOs are helping to facilitate:

- Liquidity

- Hedging

- Price convergence

- Market efficiency.

Next Steps

Look out for our last post in this series where we will discuss some of the physical and financial power market trading types.

See how you can become an energy trader and learn more about traders' critical role in the market.

For more information on the terms in this blog post, check out the Yes Energy Glossary.

Yes Energy’s tools help financial and physical traders alike!