Share this

by Rob Strange and Laura Fletcher

The Pennsylvania-New Jersey-Maryland Interconnection (PJM) capacity auction, which took place in July for the delivery year starting June 1, 2025, delivered historically high capacity prices.

Among other market signals, the high capacity prices indicate tight supply and demand conditions in the PJM region. While demand is increasing, the remaining capacity resources in the capacity auction supply stack are dwindling. PJM is experiencing an unprecedented amount of retiring capacity due to both regulatory policy and economics.

Let’s explore the drivers of high retirement rates and their implications for the PJM grid as a whole.

While federal and state environmental policies pressure thermal generations to retire, the same units still provide significant reliability to the grid. With tight supply and demand conditions, deactivating thermal power plants will trigger reliability violations unless remedial measures are created. PJM will ensure reliability and work with deactivating units in parallel with the new committed generation.

Competitive markets are evolving to address market conditions, but can they keep pace with the risks associated with PJM’s resource adequacy challenges?

PJM Plant Retirements Are Outpacing New Supply, Raising Reliability Concerns

Rate of Retirements

One of PJM’s primary roles is balancing supply and demand on the system. If incremental load (demand) is added to the system without incremental supply to match it, the balance of the system is impacted. Currently, not only is the load expected to increase but the supply is decreasing due to the rate of retirements on the system. According to the PJM’s 2023 Regional Transmission Expansion Plan (RTEP), we can anticipate around 40 GW to retire by 2030 (21% of the PJM interconnection installed capacity). Of the 40 GW, 12 GW are announced retirements, 25 GW of potential policy-driven retirements, and 3 GW of potential retirements.

The current pace of new supply is out of balance with the incremental pace of retiring resources. The rate of new supply forecast is speculative depending on the effectiveness of the interconnection queue reforms in clearing the backlog and interconnecting new resources. PJM is currently working with the Federal Energy Regulatory Commission (FERC) and stakeholders to reform the interconnection queue process. Many inefficiencies exist in the current landscape of processing many intermittent and energy storage projects in the current process, which was originally designed for large thermal resources.

Redesigning existing market mechanisms and financial products takes time, but time isn’t on PJM’s side. Before the market can successfully reform new capacity resources analyzing the appropriate steps to obtain capacity interconnection rights (CIRs), market signals have been inhibiting the pace of retirement, despite economic and policy pressure.

An overwhelming amount of intermittent generation projects in the queue are attempting to replace thermal generation. However, the power markets have reached a critical juncture in the energy transition where both PJM and market stakeholders need more time to configure their systems and processes to reach a high penetration of intermittent and energy-limited resources.

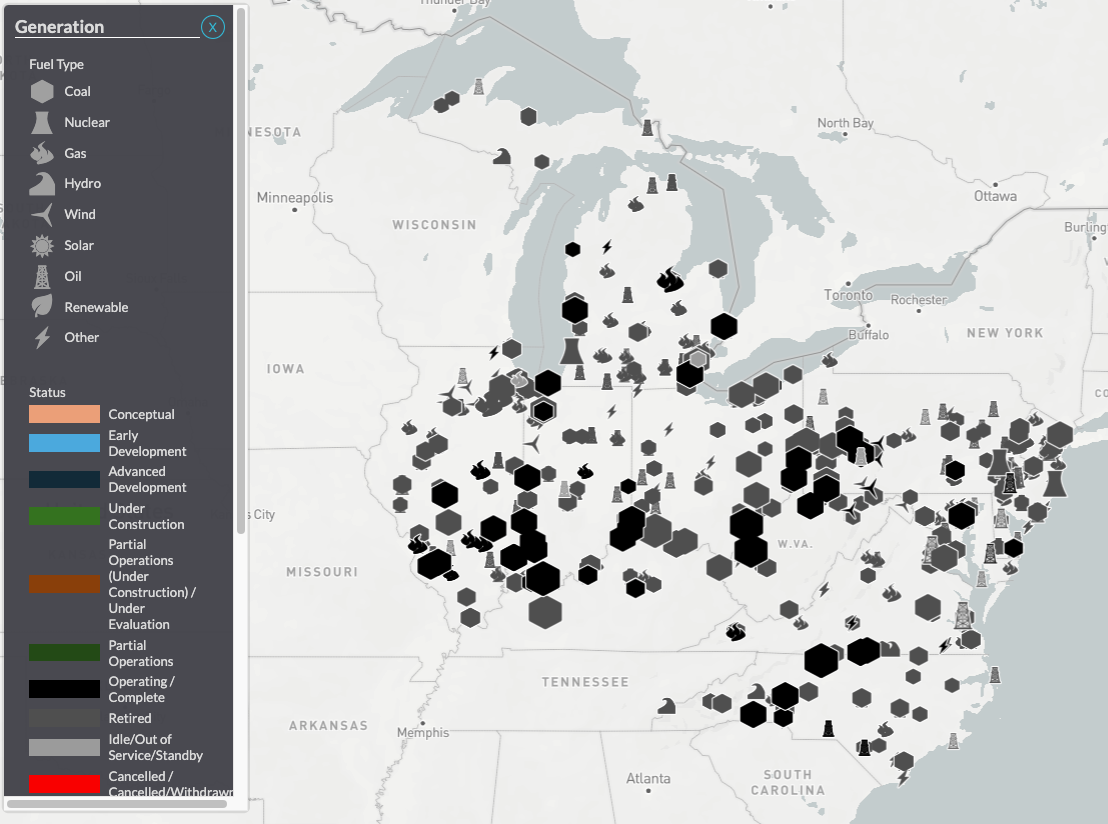

The Infrastructure Insight's map below shows the scale and magnitude of recent and projected power plant deactivations across PJM.

Source: Yes Energy’s Infrastructure Insights. Retirement projects are currently organized by states that PJM operates in.

Though future retirements are inevitable, exactly when these plants will deactivate is uncertain. As the reserve margin continues to decrease, PJM will do its best to maintain reliability as the interconnection queue process improves to displace deactivated MWs with new supply.

Plant owners will consider retiring their units if the forecasted net profit can’t cover the fixed avoidable costs over the resource’s remaining life. Many aging resources will participate less in the energy market because production costs can’t compete with other resources.

However, there’s still value in these resources during irregular conditions. Many aging fossil fuel plants can maintain net profit with revenue earned from PJM’s capacity auction, known as the reliability pricing model (RPM).

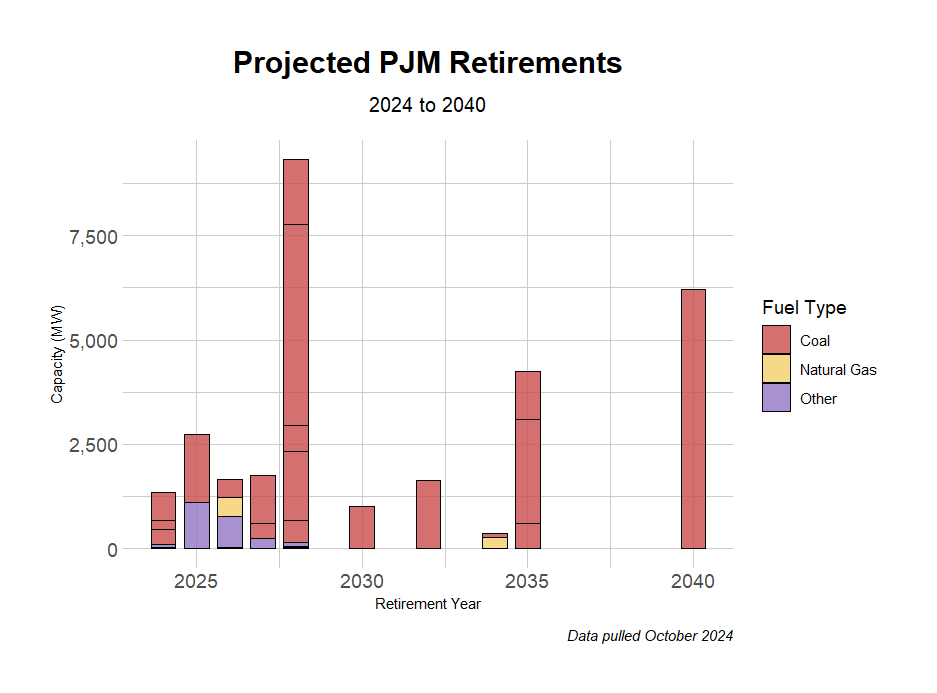

Infrastructure Insights pulls data across many sources into a single source of truth for comprehensive reporting in North America. In the graph below, data from Infrastructure Insights shows plants that indicate when they plan to deactivate given current market conditions. If capacity clearing prices remain high in upcoming auctions, this market signal may prolong retirements. For instance, many 2028 projected coal retirements may be pushed out to 2030 or later, depending on how stringent the state’s emissions goals are. which might also impact state and federal emissions goals as less time is available to reach the target.

Source: Yes Energy’s Infrastructure Insights

Diminished Energy Revenues for Thermal Resources

Many policy drivers affect the economics of resource retirements, including federal policy environmental standards and states' regulation and clean energy goals spanning 13 states and Washington, DC, in the PJM region.

PJM acknowledges the upward pressure to deactivate thermal resources largely based on state and industry environmental targets, plus economic pressure from resource developers with access to capital for clean energy resources with the state's budget from the Infrastructure Act and Inflation Reduction Act.

Several key environmental policies impact thermal resources’ net profit. Six federal US Environmental Protection Agency (EPA) policies will attempt to halt all coal-firing operations and require pollution control technology from any operating plants with nitrogen oxide (NOx) emissions.

Potential Changes to Policy Under Trump Administration

Starting in January, with Donald Trump returning to the White House and Republicans holding unified control of both congressional chambers, these policies are expected to face significant challenges, potentially becoming less effective or being fully rescinded. Trump is likely to pursue the rollback of EPA regulations by seeking court orders to remand existing rules, enabling his newly appointed EPA Administrator, Lee Zeldin, to repeal or revise the regulations.

Though federal policy will create uncertainty over the next two years as the regulatory agenda course is reversed, many of the 13 state policies will continue their plans to phase out fossil fuel-fired electric generating units (EGUs) based on carbon dioxide (CO2) and other emission limits. If the EGUs continue to operate and meet compliance based on their emission output relative to capacity size, generation owners will need to have confidence in a stable capacity revenue market when deciding whether to invest in pollution control technology. As seen in the graph above, coal can still be in operation as late as 2040. West Virginia and other states that have relaxed state emission policies will remain in operation as long it is economically viable and how federal policy is governed.

In addition to policy-related pressures, the thermal generation fleet is aging, requiring increased maintenance costs and leading to deteriorating unit economics.

Though thermal resources are retiring at an unprecedented pace, they still provide the majority of reliability services in PJM. The success of shale in the US and especially PJM has created economic opportunity and security for domestic energy prices.

Often referred to as the “fossil fuel trap,” the past success of shale has become a liability since PJM’s reliance on large-scale thermal generation makes a high penetration of clean energy resources challenging to achieve. Natural gas has served as an adequate transition fuel due to fewer carbon emissions relative to coal and oil, but it can’t achieve zero emissions goals.

The capacity and ancillary services markets still rely heavily on thermal generation – they cannot all drop off the system without new supply. Therefore, retiring generators can trigger reliability violations. If reliability violations aren’t mitigated by the time the plant plans to deactivate, PJM may offer the plant a reliability-must-run (RMR) contract to remain in operation until the plant can mitigate the reliability concerns through network upgrades or other necessary operational measures.

The PJM Deactivation Process

This leads us to the process of how a generating unit can deactivate from the bulk electricity system. If a generator-owner wishes to deactivate their plant, they have to submit a form deactivation request to PJM which is now considered announced retirement.

PJM has 60 days to respond to the generator-owner’s request after the end of the quarter in which they received the request. During that time, PJM’s Transmission Expansion Advisory Committee (TEAC) conducts a deactivation study. Generator deactivations alter power flows that can cause transmission line overloads and reduce voltage support from the generator's contributions toward reactive support.

Simply put, deactivation reliability studies include thermal and voltage analysis, common mode outage, N-1-1 contingency analysis, and load deliverability tests. The results are communicated back to the generator-owner identifying any reliability violations that they need to address through upgrading existing facilities, adding new transmission facilities, or expanding existing baseline projects.

If PJM can’t achieve the proposed mitigations in time, PJM may ask the owners to withdraw the request to deactivate and remain in operation in RMR status, since PJM can’t force a generator to stay in operation. Furthermore, PJM can’t approve a deactivation; they can only indicate reliability violations and a plan to remedy the violations.

Reliability Transmission Projects

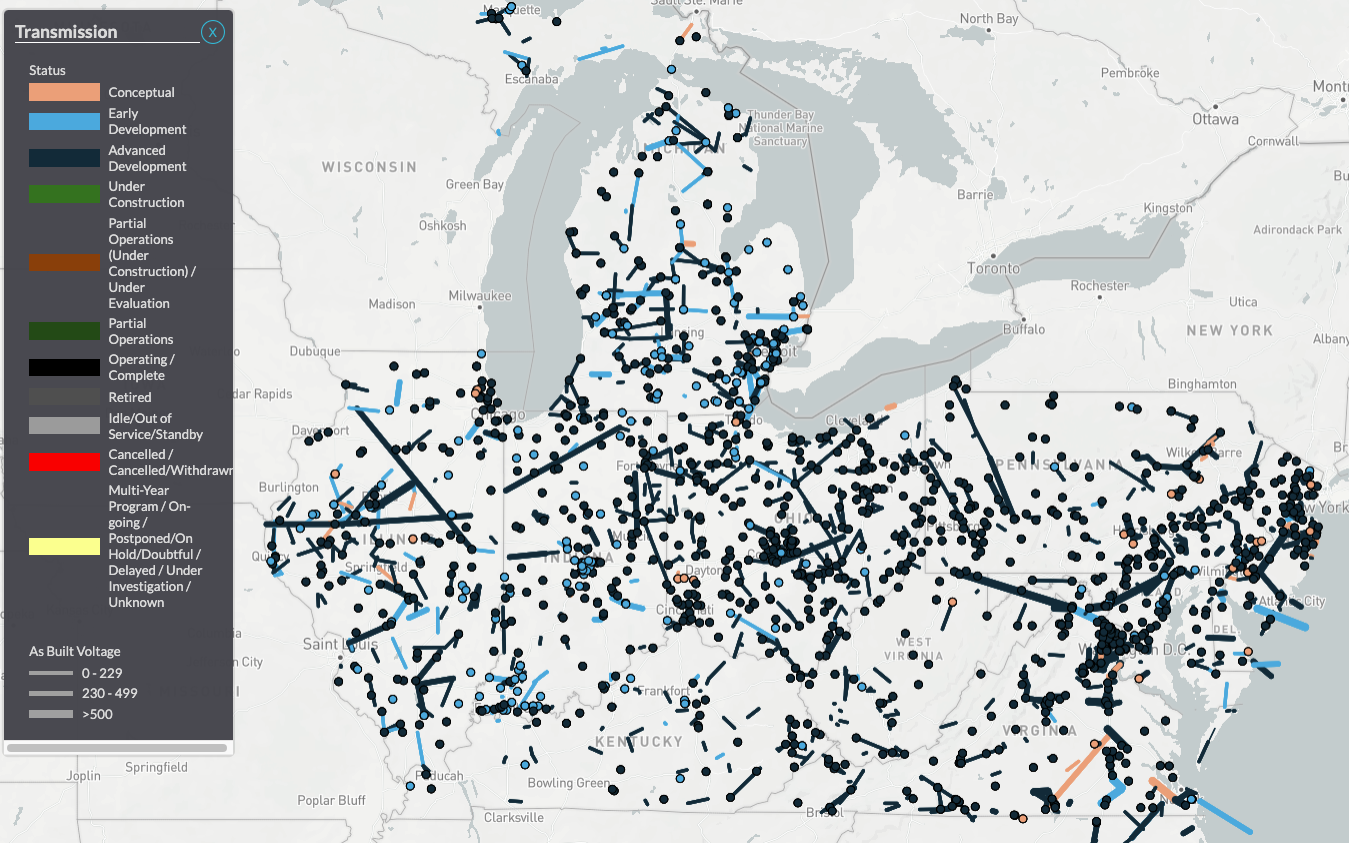

PJM will attempt to solve reliability criteria violations in the most cost-effective way to keep energy costs competitive. Due to the high rate of currently planned retirements from Infrastructure Insights (above), this can also help users understand the associated scale of upcoming changes to the transmission network. The transmission projects’ temporal and spatial information can indicate impacts on timing and proximity to upcoming related projects. This can also impact related long-term monthly trade positions for price nodes on network paths that need to be remapped.

Source: Yes Energy’s Infrastructure Insights. Retirement projects are currently organized by states that PJM operates in.

Capacity Interconnection Rights (CIR) Transfer Efficiency

The high rate of retirement provides an opportunity for new resources to interconnect to the system. PJM is proposing an updated process to transfer CIRs from deactivated units to new supply. This will create an incremental and expedited path for new supply, in addition to the lengthy process and time typically required to go through the current interconnection queue.

Generation owners considering retiring their units will have the option to transfer their CIR for a seamless transition to a new generation unit. All fuel types, including storage, are eligible to replace existing plants’ sites. To circumvent a detailed CIR study and maintain reliability and safety, the interconnection must connect at the same voltage level and the maximum facility output (MFO) can’t exceed the deactivation unit’s MW.

Besides the interconnection queue, transferring CIRs will create additional opportunities for new generation to displace deactivated megawatts by providing another option for new supply to enter the market.

However, this policy is being vetted due to concerns over potential negative consequences. PJM stakeholders have concerns that the deactivating plant owners can exert market power by withholding CIRs to the highest bidder. Also, owners of the transferred CIRs will have the advantage over new plants going through the interconnection queue seen as “queue jumping.” The traditional process of obtaining a new CIR through the interconnection queue requires lengthy studies and permitting, which wouldn’t be required for resources that would get a transferred CIR.

The committed new capacity is responsible for 100% cost allocation of required network upgrades and studies to obtain a new CIR. Similarly, the deactivating unit would be responsible for the cost related to the deactivation reliability studies. This means when the CIR is transferred to a new supply, efficiency can be realized in both deactivation reliability violations and new supply market barriers.

Conclusion

The value of capacity interconnection rights is high and only increasing as reliability becomes more at risk, especially in areas like Northern Virginia with large load centers. As reliability becomes increasingly sensitive to every interconnection, violations will be increasingly cost-effective to implement when prioritizing all transmission projects. Understanding the market solutions matters; they will affect how decisions are made in a cost-benefit analysis to achieve resource adequacy goals.

While phasing out old retiring capacity resources, the market is attempting to create new types of configurations to meet new energy loads. However, reliability must remain a top priority for grid services. At Yes Energy, we recognize that location matters and new reliability concerns will impact business decisions and modify congestion revenues.

How Can You Stay Informed?

Yes Energy’s Infrastructure Insights can help you plan for the future by seeing all announced retirements and resources planned to come online. The Infrastructure Insights Dataset is the deepest, most thoroughly researched database of all energy infrastructure projects in North America. This enhanced interconnection queue data gives you access to deep insights into the ever-changing status of planned generation, transmission and distribution, and load center (e.g. industrial, data centers, bitcoin) facilities coming online or retiring across the US and Canada.

Yes Energy’s internal Market Monitoring Team is an integral part of our commitment to better data, better delivery, and better direction. The team works year-round to analyze industry trends and upcoming policy and market redesign to ensure our products and our customers can make better decisions.

Want to stay informed on the latest ISO and RTO updates?

About the author: Rob Strange has over 10 years of experience in analytics and product development for energy solutions. His specializations include integrated DER grid benefits and resource planning by modeling grid capacity, economic conditions, and end-use characteristics. Rob is a senior market analyst on the market monitoring team at Yes Energy, leveraging his analytic experience to track and evaluate how regulatory changes impact energy market data and related market signals.

About the author: Laura Fletcher is on the Yes Energy product team as an associate product manager. Prior to joining the team, Laura studied environmental engineering at Georgia Tech. She started working with energy data as a college intern and she has worked on various consulting projects, annual market forecasts, client relations, and database management.