Share this

Increased energy storage is one of the most promising ways to handle the difficulties that come from introducing huge amounts of non-dispatchable generators to the grid. In the last two years, the number of projects on the grid has skyrocketed, and utility-scale battery energy storage system market conditions are evolving quickly.

Understanding energy storage additions to the grid is critical for a broad spectrum of market participants, from asset developers to traders to independent power producers (IPPs). The two keys to maintain project profitability are battery siting and dispatch optimization. In this blog, we’ll discuss the challenges of battery siting and operation including regulatory changes and market developments affecting price volatility.

A Battery Storage Market Forecast

As the leading provider of data and analytic solutions for wholesale electric power markets, Yes Energy® works with developers, market participants, forecasters, and algorithm developers to provide the tools needed to site, operate, and manage utility-scale battery storage systems.

These decisions include using historical data to identify places on the grid with a promising profile for storage profitability, using data on the lines on the existing grid and proposed entrants to avoid cannibalizing return, and using current and historical data to conduct fundamental analysis on market prices to operate the battery as efficiently as possible.

.png?width=1024&height=512&name=Battery%20Storage%20(1).png)

Challenge 1: Battery Siting

Battery location is the number one determinant of profitability. Most batteries on the grid today are co-located with solar or wind generators to take advantage of low prices when renewable generation is high and demand is low. Batteries in renewable-rich regions can avoid curtailment and ensure the delivery of carbon-free electricity.

Battery developers look for locations where the intra-day price volatility makes cycling the battery as profitable as possible. These conditions depend on the installed generation capacity, transmission system, and system conditions that can vary by season or even day of the week.

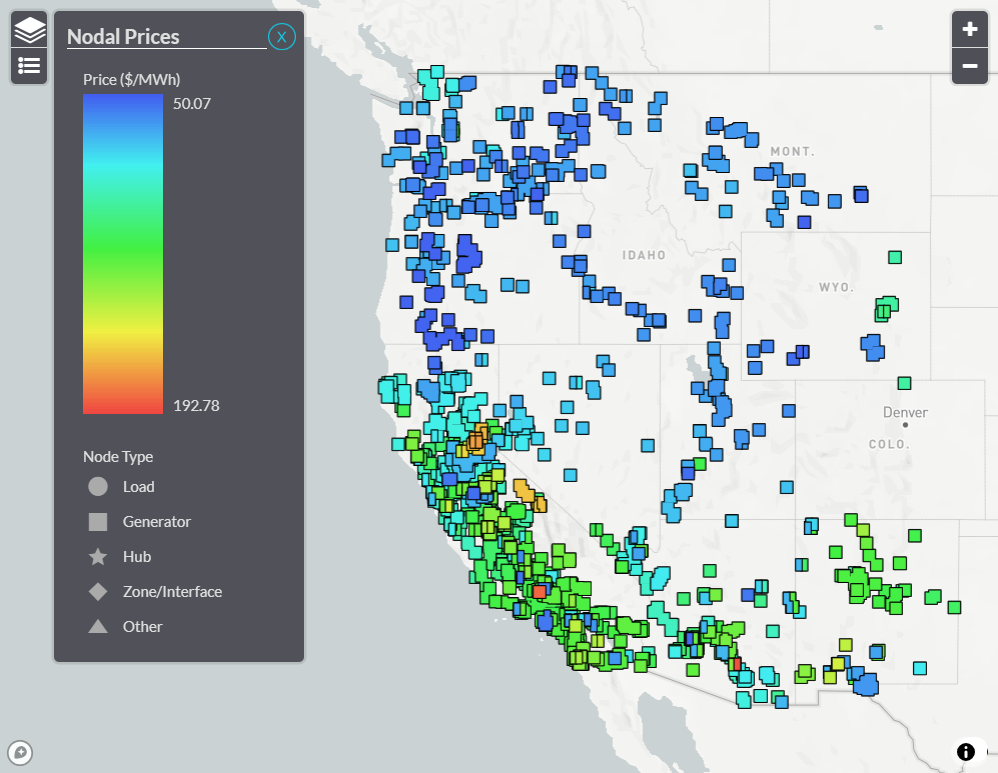

Market participants can use PowerSignals to understand historic intra-day price volatility across all nodes in CAISO over multiyear time spans (below), see how this volatility has changed over time, and then understand what market fundamentals (ex: load, wind, solar) have driven that volatility.

2023 Average Daily RT Price Ranges, CAISO and EIM Nodes

Yes Energy produced a white paper describing the considerations that go into battery siting a battery. The paper walks through the questions that have to be answered and describes data sources and one approach to the analysis needed to conduct a utility-scale battery siting study.

Challenge 2: Battery Arbitrage and Which Market to Participate in

Utility-scale battery storage operators in most markets can participate in ancillary service or energy markets. Operators must weigh providing ancillary services, like synchronized reserves or frequency regulation, against participating in energy markets. Finding the optimal time to charge and discharge requires a detailed understanding of tomorrow’s market prices today.

Most importantly, operators must manage the risk of offering energy into the market while at the same time bidding to purchase that energy earlier in the day, creating correlated risks.

Battery operation requires choosing which market to participate in and when to charge and discharge the battery to maximize return while maintaining battery performance. Many existing batteries participate in the ancillary service market, providing frequency regulation and reserves. These markets are lucrative but small.

Batteries will increasingly have to turn to day-ahead real-time (DART) energy market arbitrage as a source of revenue. This strategy is as simple as charging when prices are low and discharging when they are high. As long as the price difference exceeds the round-trip cycling inefficiency of the battery, this trade is profitable. Wholesale electricity markets, renewable generators, and consumers all benefit from this trade.

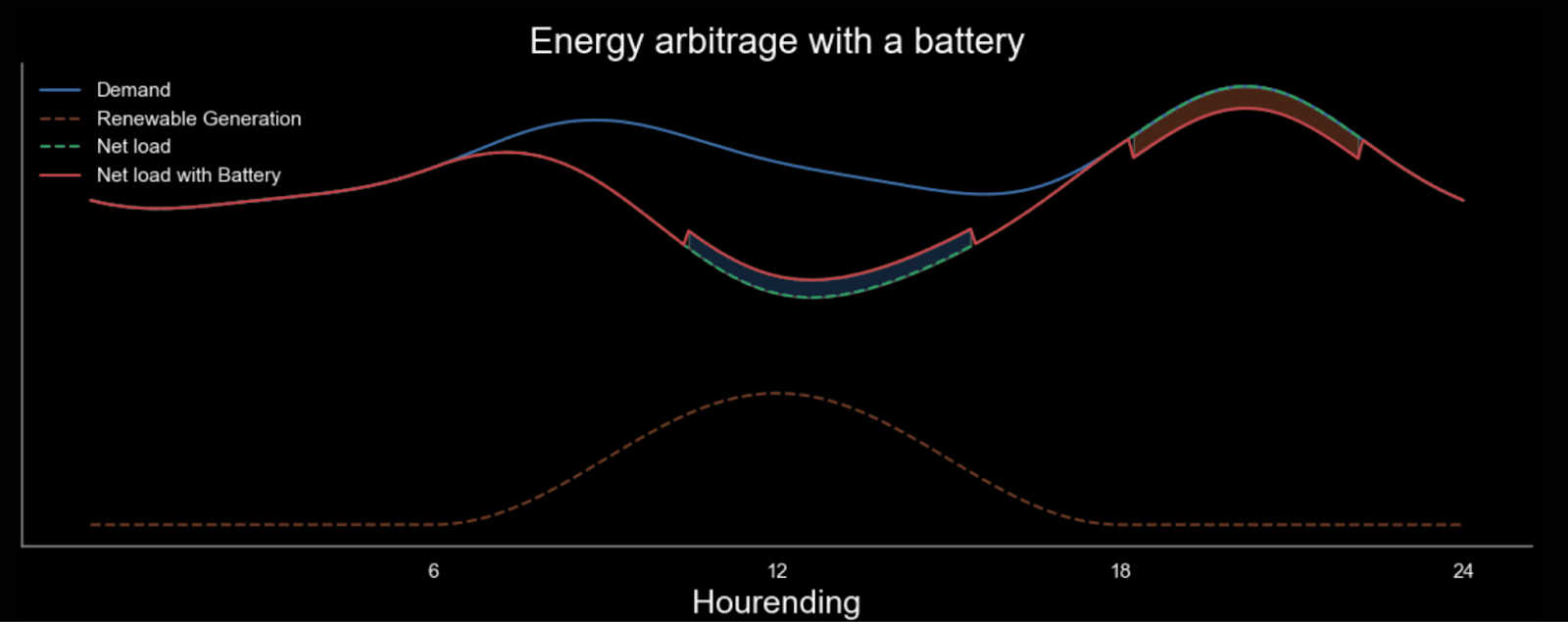

The figure below is a stylized example of how energy market arbitrage can work. The battery charges during the highest production solar hours and discharges during the evening ramping period when net demand is growing most rapidly.

Example for illustrative purposes only

The battery increases demand when it is lowest, providing an outlet for solar generation and helping manage the difficult process of rapidly increasing generation in the evening when demand is going up, just as solar generation is dropping off the grid. This allows batteries to capture low-cost, carbon-free energy and dispatch it when prices are highest.

Because of the non-linearity in electricity prices, the costs created by charging are much less than the costs offset by discharging when net demand is high, creating lower prices market-wide to eventually be passed on to consumers.

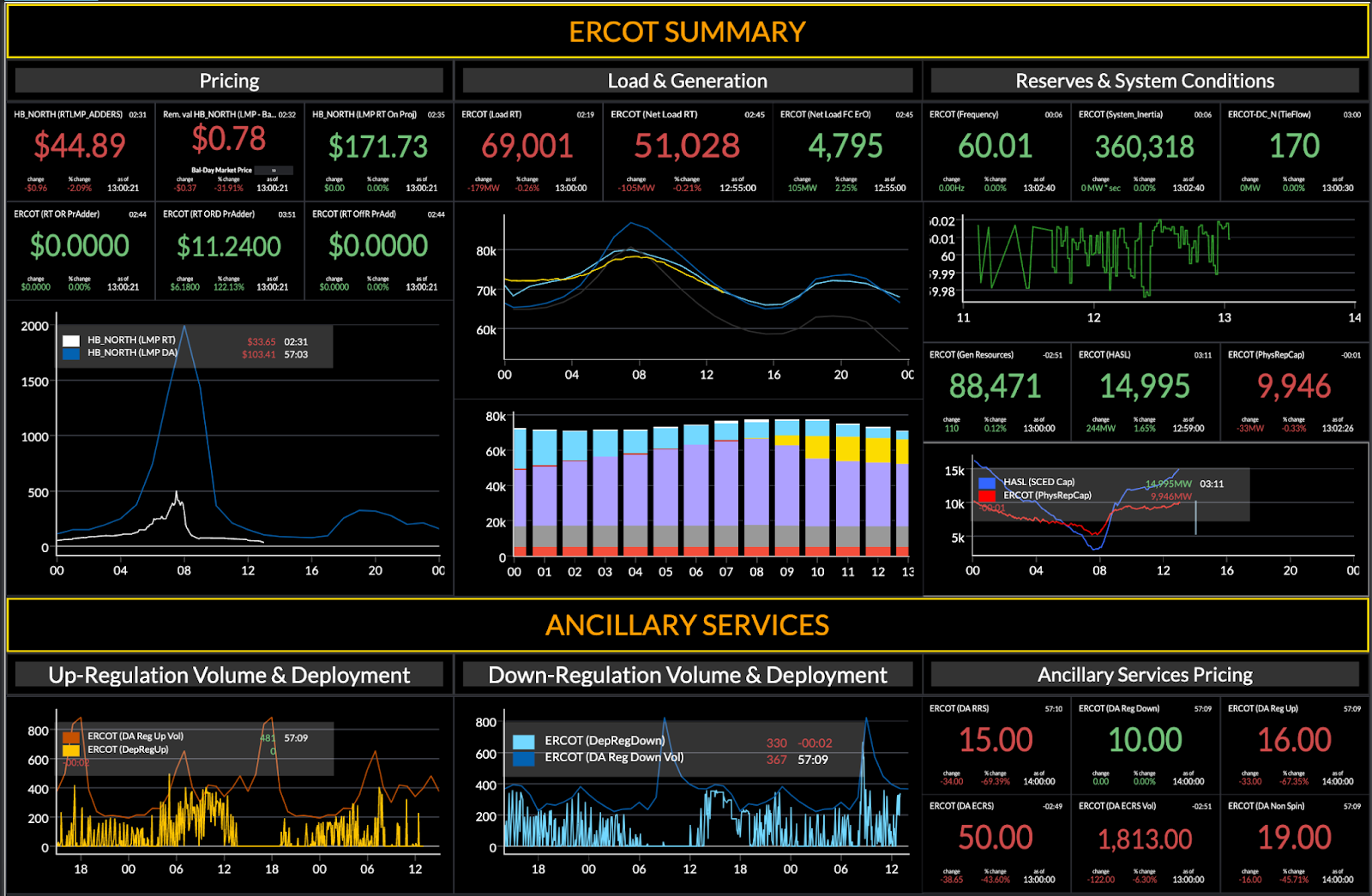

In the Electric Reliability Council of Texas (ERCOT) the most lucrative market for batteries has been the ancillary services. These services include regulation of frequency, responsive spinning reserves (RSS), non-spinning reserves, and ERCOT contingency reserve service (ECRS). The responsive spinning reserves are resources synchronized to the frequency of the grid and used to manage unexpected imbalances in supply and demand on the grid. This service is the primary revenue stream for batteries on the grid and batteries make the largest source of RSS.

In the image below, we see ERCOT data as viewed through Yes Energy’s QuickSignals module.

ERCOT data showcased in QuickSignals

The entire ancillary service market is less than five percent of the overall ERCOT market, and batteries are competing aggressively to provide those services, which is already reducing margins. As additional capacity enters the market, batteries will be forced to compete more aggressively in the energy markets.

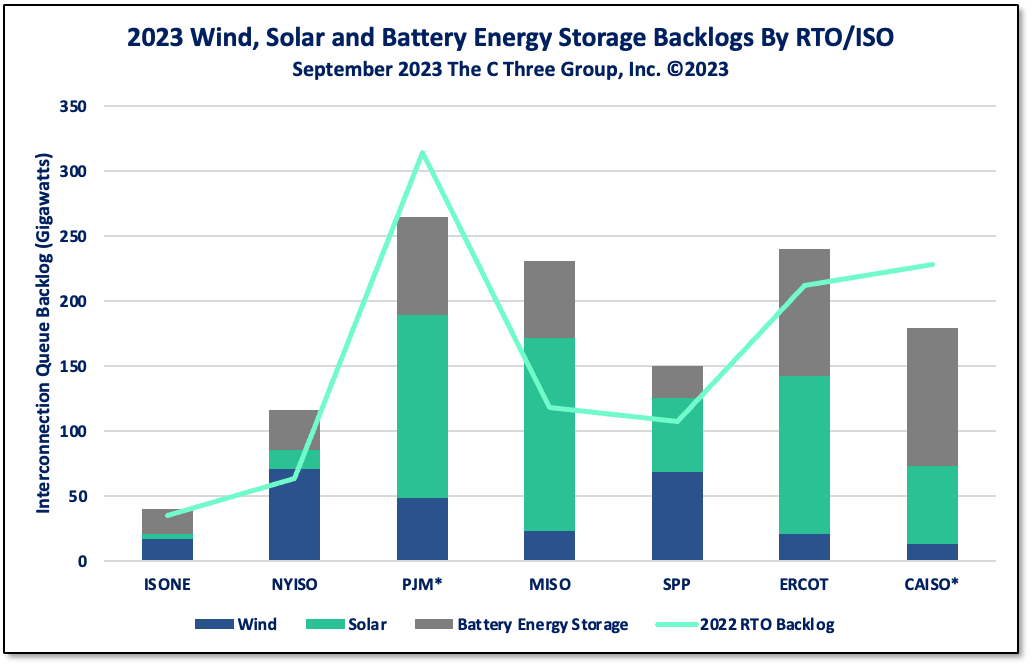

Challenge 3: Grid Backlog and Its Effects on the Battery Energy Storage Market

However, in the most volatile markets, past prices may be a poor predictor of future returns. In ERCOT, there are about 17 GWs of solar with signed interconnection agreements with plans to be online before the end of 2024. That represents a doubling of solar capacity. The amount of utility-scale battery storage capacity with interconnection agreements in place is more than quadruple current capacity. This entry will reshape the topology of the grid. Visibility into the interconnection queue is a key component of any siting analysis.

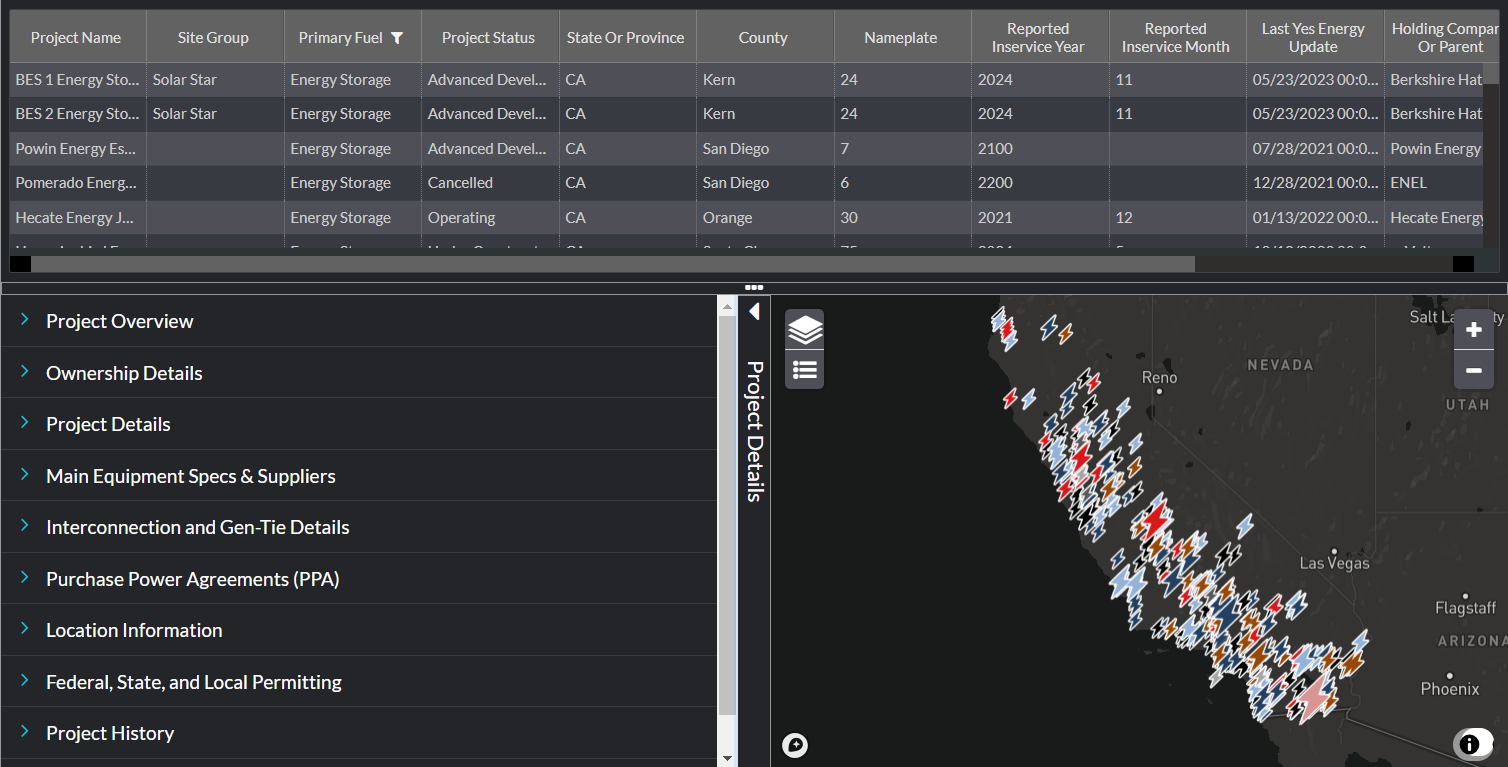

Yes Energy’s Infrastructure Insights Dataset is a tool that enables market participants to see where new utility-scale energy storage systems are being built to strengthen their siting analysis.

In the image below, we can see all upcoming and operating utility-scale battery storage projects in the California Independent System Operator (CAISO). Understanding energy storage additions to the grid is critical for a broad spectrum of market participants from asset developers to traders to independent power producers (IPPs).

CAISO data showcased in the Infrastructure Insights Dataset

The costs of installing utility-scale battery storage systems have plummeted over the past five years, making them cost competitive with other generation technologies. The falling costs have been associated with explosive growth in capacity, particularly in CAISO and ERCOT.

The interconnection queues are full of additional renewable and storage generators. Currently, there are 110 GWs of solar and 90 GWs of storage waiting for approval. While some of this capacity may never be built, it sends a strong signal that market participants see potential for storage.

RTO/ ISO energy storage backlog by C Three Group, now a part of Yes Energy

Regulatory Changes

FERC Order 841 required regional transmission operators (RTOs) and independent system operators (ISOs) to facilitate the participation of electric storage in their markets. Long interconnection queues, supply chain difficulties, and uneven enforcement of market rules have been a drag on the installation of batteries.

Despite these headwinds, market logic has driven quickly increasing capacity, particularly high-renewable-penetration markets.

FERC order 841 required ISOs to provide non-discriminatory access to electric storage providers. The order required “each RTO and ISO to revise its tariff to establish a participation model consisting of market rules that, recognizing the physical and operational characteristics of electric storage resources, facilitates their participation in the RTO/ISO markets.”

The ISOs have employed different strategies to comply with the order. The market rule changes have taken a long time to implement and don’t seem to be the primary driver of increased storage capacity on the grid. As these rules are implemented and developers respond, the order may still facilitate storage expansion, but the effects are likely years away from being felt.

There have been some policy changes that will encourage additional storage capacity.

In ERCOT, the Texas state legislature has passed several laws that will affect storage. HB15000 requires the creation of a new ancillary service product for dispatchable reserve, and storage operations should be eligible to participate in that market. SB2627 provided billions of dollars in subsidies for dispatchable generation. It does not appear that storage will be eligible for most of the funding, but nearly $2 billion was set aside for microgrids that may include energy storage.

Challenge 4: Battery Component Price Volatility

The demand for chemical batteries has skyrocketed, driving component prices to historic levels. Lithium-ion batteries are likely to remain the dominant technology for several years. These batteries rely on minerals like cobalt, copper, lithium, magnesium, and nickel. These minerals are mined in a handful of countries and largely processed in China.

The US mines almost none of these minerals, accounting for around three percent of global lithium production and less than one percent of the rest. The prices of rare earth minerals have been volatile over the last few years, and Chinese export restrictions, pandemic-induced distribution challenges, and large demand increases have buffeted the sector.

Source: https://www.lexology.com/library/detail.aspx?g=19f6adb5-1a68-41d1-a95b-dce047b5feb8

There are few prospects for short-run price stability. Developing new sources of minerals is extremely expensive and, in the US, faces long permitting delays. In the medium term, new technologies that rely on substitutes for lithium will become price and performance competitive. High prices have led several mothballed lithium mines to restart production. These new sources of supply and competition from new technologies will eventually stabilize the price of these crucial minerals.

Other Profitability Threats

Solar and wind projects were developed in profitable locations based on historic pricing, but the huge amount of renewable entry led to low and occasionally negative prices in those areas, hurting project return. The huge growth in battery capacity also risks cannibalizing returns in ancillary service markets and transmission-constrained portions of the grid.

Understanding current project economics and risk associated with future changes in the structure of the grid-driven load, generation, and competing storage is becoming increasingly important.

The amount of storage in the interconnection queue in ERCOT swamps the size of the ancillary service markets in which storage can participate. New entrants and existing facilities will need to find additional sources of return, most likely by pairing with renewable generators to take excess production during times of low demand or by participating in the DART power markets.

One source of expanded demand for storage may be as a substitute for transmission capacity. Transmission expansion is desperately needed to move renewable energy to load, facilitating additional capacity.

The cost and political difficulty of installing new transmission have slowed progress. Multiple ISOs are exploring storage as transmission projects that allow existing transmission capacity to be used more intensively.

Storage as transmission will require new market designs, but in some parts of the grid, storage may alleviate transmission bottlenecks and allow renewable energy to access load, reducing congestion and costs.

Conclusion

Market conditions are evolving quickly for utility-scale energy storage. In the last two years, the number of projects on the grid has skyrocketed. These projects are paired with renewables, typically solar, to take excess generation and avoid curtailment. A growing number are taking advantage of lucrative ancillary service markets.

Market operators have been slow to implement rules facilitating battery participation, but this has not slowed the introduction of new projects or applications to interconnect additional capacity.

In the short run, battery component price volatility has the potential to affect costs, but in the longer run the outlook for new technologies and new sources of supply reduces risks. More concerning is potential cannibalization from large amounts of new capacity competing margins away.

The two keys to maintain project profitability are battery siting and dispatch optimization. Siting requires understanding historic patterns of congestion and how new entrants will affect the topology of the grid. Battery optimization requires insight into market conditions that will drive intra-day price volatility so operators can manage their charging and discharging cycle.

Yes Energy’s Infrastructure Insights Dataset allows market participants to unlock deep insights into the ever-changing status of planned generation, transmission, and load center facilities coming online or retiring across the US. The Infrastructure Insights Dataset is the deepest and most thoroughly researched database of all energy infrastructure projects in North America.

Request a demo to see how your organization can better understand upcoming projects affecting the power grid, including battery energy storage systems.