Share this

by Tim Hough

On September 26, 2024, the West-Wide Governance Pathways Initiative released its Step 2 draft proposal. This follows the approval of Step 1 in the West-Wide Governance Pathways Initiative by the California Independent System Operator (CAISO) Board of Governors and the Western Energy Market (WEM) Governing Body on August 13, 2024, marking yet another significant development between the Western Interconnection’s developing energy markets.

The developments in the Pathways Initiative have sent ripples throughout Western market participants, most of whom are still determining which developing Western day-ahead and real-time market to join: CAISO’s EDAM or SPP’s Markets+.

Perhaps the most notable entity that continues to assess the benefits to be gained from one of these markets is Bonneville Power Administration (BPA), an American federal agency that owns and operates 75% of the Pacific Northwest’s high-voltage transmission capacity.

Let’s explore BPA’s history in the US energy markets in the West, the latest regulatory developments, and their potential impacts.

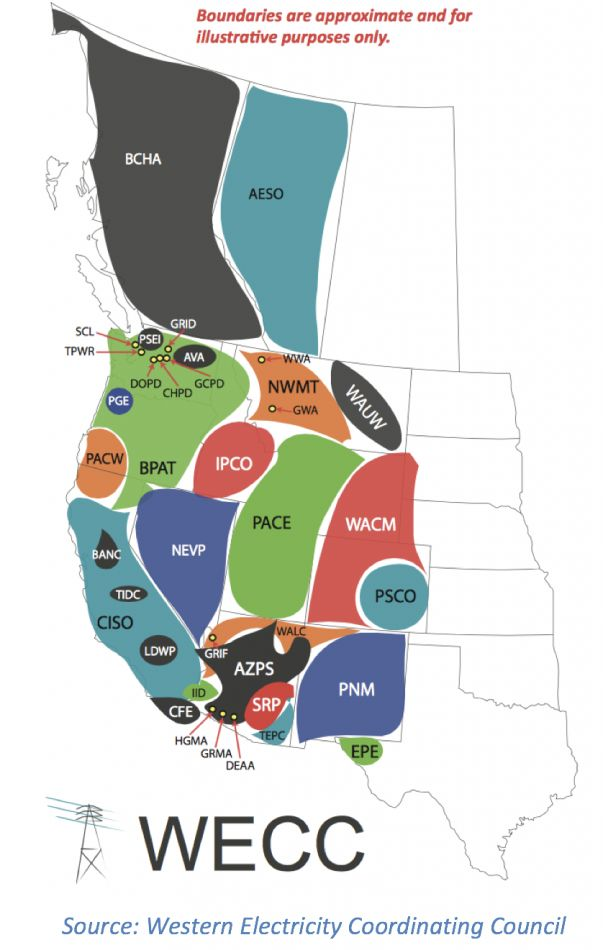

Balancing authority areas of the Western Interconnection. Source: Western Electricity Coordinating Council (WECC).

Overview of the Developing Western Markets

Both CAISO’s EDAM and SPP’s Markets+ will introduce day-ahead markets to the West, expanding the benefits that the current real-time markets, CAISO’s WEIM and SPP’s WEIS, bring to the region through optimizing existing transmission and generation resources over a larger time frame. They’re committing least-cost generation across their respective footprints to enhance reliability, economic, and environmental benefits to Western utilities and customers.

One key difference between the two prospective markets, however, is their governance.

SPP’s Markets+ was designed around its fully independent governance structure, with oversight from SPP’s independent board of directors and the Markets+ Independent Panel, which provides all participants with equal opportunity to contribute to the market’s development and structure.

CAISO’s EDAM, meanwhile, is jointly governed by CAISO’s Board of Governors, appointed by California’s governor, and the WEM (formerly WEIM) Governing Body. Since CAISO’s Board of Governors have obligations to California ratepayers, unlike Markets+, EDAM wasn’t fully independent from any one state before the approval of Step 1 in the Pathways Initiative. EDAM is set to launch in spring 2026.

EDAM, which began development earlier than Markets+, had its tariff approved by FERC in December 2023. SPP filed the Markets+ tariff with FERC in March 2024, but received a deficiency notice on July 31, with FERC requesting additional clarity on 16 issues found within the tariff. While this notice delays the launch of Phase 2, SPP said that FERC broadly accepted the market design and that SPP accounted for delays in the development timeline, so this will not delay the slated early 2027 launch for Markets+. SPP submitted its response to FERC’s deficiency letter on September 20, 2024, requesting that FERC issue an order on the Markets+ tariff revisions by November 20, 2024.

Background of the Pathways Initiative

The Pathways Initiative, launched in October 2023, moves to establish an independent regional organization to govern CAISO’s Extended Day-Ahead Market (EDAM) and Western Energy Imbalance Market (WEIM), which previously gave CAISO’s Board of Governors primary decision-making authority. Notably, California’s governor appoints CAISO’s Board of Governors, and they have obligations to California ratepayers. This causes many prospective EDAM participants to question whether they would have fair representation in the developing market.

The Step 1 approval began a process that will give the WEM Governing Body primary decision-making authority over the two markets. A committee of Western energy stakeholders nominate members of the WEM Governing Body. This governance change won’t trigger until the EDAM obtains implementation agreements from a set of geographically diverse non-CAISO EDAM Entities from the Northwest and Southwest that represent at least 70% of CAISO’s annual load in 2022, which was 210,879 GWh.

While only a draft, the Step 2 draft proposal would remove any remaining unilateral authority that CAISO’s board still had, following Step 1. This would create a regional organization (RO) that essentially assumes the role of the WEM Governing Body, giving full authority over market rules, making most FERC filings and business practice manual provisions. RO and CAISO rules will exist within a single integrated tariff, but CAISO’s board will retain some authorities, specifically relating to the ISO’s balancing authority or grid. This includes the ISO performing day-to-day market operations. These proposed changes under Step 2 will require a change to California law, which has historically proven to be a large undertaking. This draft proposal leaves the option for the RO to assume more of CAISO’s market functions and legal responsibilities, but that transition would occur over several years, following the implementation of Step 2 of the Pathways Initiative.

A timeline of relevant Markets+ (blue), EDAM (orange), and BPA (yellow) developments

Bonneville Power Administration Delays Decision

In April 2024, BPA announced its plans to release a draft decision on its Western day-ahead market decision, slated for release on August 29. BPA’s eight market evaluation principles govern this choice. These include statutory, regulatory, and contractual obligations; service reliability to its customers; resource adequacy frameworks to ensure system reliability; business rationale; consistency with BPA’s strategic plan; independence and inclusivity in governance structure; commercial and operational impacts to customers; and greenhouse gas emission impacts.

On August 22, 2024, just nine days after Step 1 of the Pathways Initiative was approved, BPA delayed its market decision.

This is significant in at least two ways.

First, BPA’s market decision will impact the outcome of CAISO’s EDAM and SPP’s Markets+ current and prospective participants, as BPA’s decision will define the seam that forms between the two markets. BPA has, and continues to face, pressure from supporters of both markets because of the market decisions of its neighbors and pleas from BPA’s customers, utility regulators, and even Pacific Northwest Congress members.

Second, with the market decision being delayed, the realization of economic benefits for customers across the Pacific Northwest and the Markets+ footprint could be affected, as these benefits would largely depend on BPA's funding for Phase 2 of the Markets+ development. Phase 2, which can’t begin until FERC approves the Markets+ tariff, will implement the Markets+ design from Phase 1 and integrate participants into the market.

A map of the potential footprints, excluding BPA’s service territory (yellow) to highlight the potential market seams of EDAM (blue), based on utilities that have joined, or signaled their intent to join EDAM, and Markets+ (orange), based on its Phase 1 participants. Note: many Markets+ Phase 1 participants are utilities located within BPA’s footprint.

According to an email on August 26, BPA is delaying this draft decision until March 2025, with a final decision in May, to allow for a more informed decision on potential market participation for the good of BPA’s customers and the Pacific Northwest region.

BPA was a contributor to the development of both Markets+ and EDAM. On April 4, 2024, BPA released a staff report recommending Markets+ over EDAM. The primary difference maker highlighted in that report was the governance structures used between the two markets, with the independent governance structure of Markets+ making it seem like a potentially better long-term market to join. Additionally, Markets+ requires participants to join the Western Power Pool’s Western Resource Adequacy Program (WRAP), which BPA viewed favorably. SPP operates the WRAP, and it’s the dominant Western resource adequacy program outside of California.

Notably, BPA was adamant that its staff report sought to analyze the two markets without issuing a final decision or endorsement for either one. In this report, BPA also revealed plans to issue a market choice decision draft in August, followed by a final decision before the end of the year.

In July 2024, BPA ramped up its participation in the Pathways Initiative, which began moving into Step 2 of the initiative. BPA assigned staff to four of the initiative’s six new working groups, while making it clear that this doesn’t represent a change in the staff recommendation or an endorsement of EDAM or the Pathways conclusions.

BPA’s Reasons for the Delayed Decision

BPA made clear that both SPP’s Markets+ and CAISO’s EDAM have outstanding issues.

For Markets+, BPA cited the additional tariff development needed to address the deficiencies FERC found in the Markets+ tariff, which SPP addressed in its September 20, 2024 response to FERC.

For EDAM, BPA said that Step 1 of the Pathways Initiative is only an early step in the process of passing the necessary California legislation to make the WEM Governing Body the sole governing authority over the EDAM and WEIM markets. BPA has yet to publicly comment on the Step 2 draft proposal released on September 26, 2024.

BPA was initially vague, saying it will “continue to fund and commit staff resources to the Markets+ design effort.” However, BPA later clarified its intention to fund its 17.4% share of Phase 2’s estimated $150 million in implementation costs. This percentage has risen from BPA’s Phase 1 funding share of 15.2% of the $9.7 million costs due to NV Energy, Western Area Power Administration’s Desert Southwest Region, Liberty Utilities, and Arizona Electric Power Cooperative pulling their support from Markets+.

Consequently, had BPA elected to join EDAM instead and not fund Phase 2, the other Markets+ participants would have had to cover BPA’s roughly $26 million share.

Neighbors, Regulators, and Senators Pressure BPA

Many sources are encouraging BPA to join EDAM. First, two of its neighbors, PacifiCorp and PGE, formally committed to join EDAM. Second, Northwest utility regulators with no oversight authority over BPA seek to create a single market based on EDAM. Third, the four US Democratic Senators representing Oregon and Washington in a July 25 letter urged BPA to delay its market decision, stating their belief that the Northwest would benefit more from a single organized market, rather than two.

Arguing in favor of Markets+ are many of BPA’s “preference customers,” publicly owned utilities that make up its principal customer base.

Most notably, on August 21, 2024, 47 of the agency’s 149 wholesale electricity customers sent a response to the Northwestern US Senators. This letter condemned the senators’ pressure for BPA to delay making a market decision, arguing that despite the senators’ letter claiming it was not favoring one market over the other, pressuring BPA to delay its funding and participation decisions “undermines the viability of SPP’s Markets+ and favors CAISO’s EDAM.” The utilities said that the competition between Markets+ and EDAM benefit all Western participants, as the developing markets continually improve their design to entice undecided entities. This response letter also reiterated BPA’s concerns about EDAM’s California-heavy governance, placing doubt on the ability of the Pathways Initiative to change California law to allow for a truly independent governance in the EDAM, based on similar California efforts having “always failed.”

Further criticizing EDAM, this letter contended that CAISO’s current “flawed governance” that EDAM was designed under would take several years to correct market design that diminishes Northwestern interests.

The utilities thought it imperative to continue the developments of a day-ahead market that respects ratepayers’ policy, economic, and regulatory interests in Markets+, with BPA’s ongoing funding commitment essential in Phase 2 of the process.

Where Does This Leave the West?

While we wait for BPA’s decision in March 2025, SPP will most likely kick Phase 2 of Markets+, and more organizations will likely commit to joining CAISO’s EDAM.

The more commitments EDAM gets, the more pressure BPA and other undecided Western entities face.

This is particularly true for the entities that operate within BPA, which prefer to join Markets+, because they already face a large market seam to the South due to Portland General Electric and Pacificorp joining EDAM.

As the Pathways Initiative moves forward with Step 2, EDAM’s market structure continues to develop while entities begin to onboard, and Markets+ aims to enter Phase 2 of its development pending FERC’s response (SPP requested a November 20 response). BPA’s participation in the development of both aspiring markets will be closely monitored by Yes Energy's Market Monitoring team. As we move closer to the go-live dates for EDAM and Markets+, markets and regulatory changes in the west are developing quickly. Our team is tracking these changes to determine how they will impact Yes Energy customers.

Conclusion

Stay tuned for an upcoming blog on the full timeline of Markets+ and EDAM developments. If you’re wondering how the developments of US energy markets in the West could impact your business, trading decisions, and bottom line, our team of experts has you covered so you can “win the day aheadTM." Ask our team your question or subscribe to our blog to get power industry updates directly to your inbox!

About the author: Tim Hough is a market analyst on the market monitoring team at Yes Energy, specializing in the CAISO and SPP markets. He graduated from Pomona College in 2024, where he pursued his passion in the energy transition by obtaining a degree in environmental analysis and economics.

About the author: Tim Hough is a market analyst on the market monitoring team at Yes Energy, specializing in the CAISO and SPP markets. He graduated from Pomona College in 2024, where he pursued his passion in the energy transition by obtaining a degree in environmental analysis and economics.